Humana 2011 Annual Report Download - page 15

Download and view the complete annual report

Please find page 15 of the 2011 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

Our Products

Our medical and specialty insurance products allow members to access health care services primarily

through our networks of health care providers with whom we have contracted. These products may vary in the

degree to which members have coverage. Health maintenance organizations, or HMOs, generally require a

referral from the member’s primary care physician before seeing certain specialty physicians. Preferred provider

organizations, or PPOs, provide members the freedom to choose a health care provider without requiring a

referral. However PPOs generally require the member to pay a greater portion of the provider’s fee in the event

the member chooses not to use a provider participating in the PPO’s network. Point of Service, or POS, plans

combine the advantages of HMO plans with the flexibility of PPO plans. In general, POS plans allow members to

choose, at the time medical services are needed, to seek care from a provider within the plan’s network or outside

the network. In addition, we offer services to our health plan members as well as to third parties that promote

health and wellness, including pharmacy, primary care, integrated wellness, and home care services. The

discussion that follows describes the products offered by each of our segments.

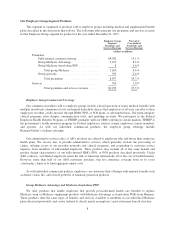

Our Retail Segment Products

This segment is comprised of products sold on a retail basis to individuals including medical and

supplemental benefit plans described in the discussion that follows. The following table presents our premiums

and services revenue for the Retail segment by product for the year ended December 31, 2011:

Retail Segment

Premiums and

Services Revenue

Percent of

Consolidated

Premiums and

Services Revenue

(dollars in millions)

Premiums:

Individual Medicare Advantage ................ $18,100 49.6 %

Individual Medicare stand-alone PDP ........... 2,317 6.4 %

Total individual Medicare ................ 20,417 56.0 %

Individual commercial ....................... 861 2.4%

Individual specialty ......................... 124 0.3%

Total premiums ........................ 21,402 58.7 %

Services ...................................... 16 0.0%

Total premiums and services revenue ....... $21,418 58.7 %

Individual Medicare

We have participated in the Medicare program for private health plans for over 25 years and have

established a national presence, offering at least one type of Medicare plan in all 50 states. We have a

geographically diverse membership base that provides us with greater ability to expand our network of PPO and

HMO providers. We employ strategies including health assessments and clinical guidance programs such as

lifestyle and fitness programs for seniors to guide Medicare beneficiaries in making cost-effective decisions with

respect to their health care. We believe these strategies result in cost savings that occur from making positive

behavior changes.

Medicare is a federal program that provides persons age 65 and over and some disabled persons under the

age of 65 certain hospital and medical insurance benefits. CMS, an agency of the United States Department of

Health and Human Services, administers the Medicare program. Hospitalization benefits are provided under Part

A, without the payment of any premium, for up to 90 days per incident of illness plus a lifetime reserve

aggregating 60 days. Eligible beneficiaries are required to pay an annually adjusted premium to the federal

government to be eligible for physician care and other services under Part B. Beneficiaries eligible for Part A and

5