Sony 2005 Annual Report Download - page 101

Download and view the complete annual report

Please find page 101 of the 2005 Sony annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

98 Sony Corporation

costs are deferred and amortized generally over the premium-

paying period of the related insurance policies, and that future

policy benefits for life insurance calculated locally under the

authorization of the supervisory administrative agencies are

comprehensively adjusted to a net level premium method with

certain adjustments of actuarial assumptions for U.S. GAAP

purposes. For purposes of preparing the consolidated financial

statements, appropriate adjustments have been made to reflect

such items in accordance with U.S. GAAP.

The amounts of statutory net equity of the subsidiaries as of

March 31, 2004 and 2005 were ¥146,540 million and ¥153,228

million ($1,432 million), respectively.

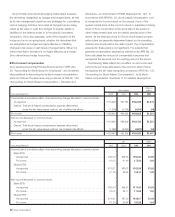

(1) Insurance policies:

Life insurance policies that the life insurance subsidiary writes,

most of which are categorized as long-duration contracts,

mainly consist of whole life, term life and accident and health

insurance contracts. The life insurance revenues for the years

ended March 31, 2003, 2004 and 2005 were ¥450,363 million,

¥437,835 million and ¥426,774 million ($3,989 million), respec-

tively. Property and casualty insurance policies that the non-life

insurance subsidiary writes are primarily automotive insurance

contracts which are categorized as short-duration contracts.

The non-life insurance revenues for the years ended March 31,

2003, 2004 and 2005 were ¥21,269 million, ¥28,371 million and

¥35,454 million ($331 million), respectively.

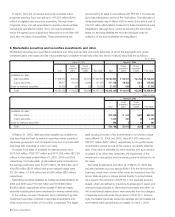

(2) Deferred insurance acquisition costs:

Insurance acquisition costs, including such items as commis-

sion, medical examination and inspection report fees, that vary

with and are primarily related to acquiring new insurance policies

are deferred as long as they are recoverable. The deferred

insurance acquisition costs for traditional life insurance contracts

are amortized over the premium-paying period of the related

insurance policies using assumptions consistent with those

used in computing policy reserves. The deferred insurance

acquisition costs for non-traditional life insurance contracts are

amortized over the expected life in proportion to the estimated

gross profits. Amortization charged to income for the years

ended March 31, 2003, 2004 and 2005 amounted to ¥44,578

million, ¥50,492 million and ¥47,120 million ($440 million),

respectively.

(3) Future insurance policy benefits:

Liabilities for future policy benefits are established in amounts

adequate to meet the estimated future obligations of policies in

force. These liabilities are computed by the net level premium

method based upon estimates as to future investment yield,

morbidity, mortality and withdrawals. Future policy benefits are

computed using interest rates ranging from approximately

1.30% to 5.20%. Mortality, morbidity and withdrawal assump-

tions for all policies are based on either the subsidiary’s own

experience or various actuarial tables. At March 31, 2004 and

2005, future insurance policy benefits amounted to ¥1,605,178

million and ¥1,782,850 million ($16,662 million), respectively.

(4) Separate account assets:

Separate account assets are funds on which investment income

and gains or losses accrue directly to policyholders. Separate

account assets are legally segregated. They are not subject to

the claims that may arise out of any other business of a life

insurance subsidiary. As described in Note 2, the AcSEC issued

SOP 03-1, “Accounting and Reporting by Insurance Enterprises

for Certain Nontraditional Long-Duration Contracts and for

Separate Accounts”. As a result of the adoption of SOP 03-1 on

April 1, 2004, the separate account assets, which are defined by

insurance business law in Japan and were previously included in

“Securities investments and other” (Note 8) in the consolidated

balance sheet, were excluded from the category of separate

accounts under the provision of SOP 03-1. Accordingly, the

assets previously treated as separate account assets are now

treated within general account assets. The related liabilities are

treated as policyholders’ account and included in future insur-

ance policy benefits and other in the consolidated balance

sheet. Fees earned for administrative and contract-holder

services performed for the separate accounts are recognized as

financial service revenue.

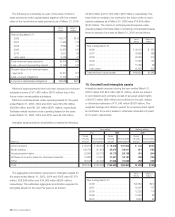

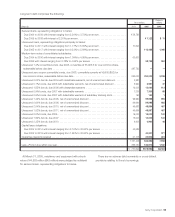

12. Short-term borrowings and long-term debt

Short-term borrowings comprise the following:

Dollars in

Yen in millions millions

March 31 2004 2005 2005

Unsecured loans,

principally from banks:

with weighted-average

interest rate of 1.80% . . .

¥26,260

with weighted-average

interest rate of 2.79% . . .

¥38,796 $362

Secured call money:

with weighted-average

interest rate of 0.01% . . .

65,000 ——

Secured bills sold:

with weighted-average

interest rate of 0.00% . . .

—24,600 230

. . . . . . . . . . . . . . . . . . . .

¥91,260 ¥63,396 $592

At March 31, 2005, marketable securities and securities

investments with a book value of ¥27,433 million ($256 million)

were pledged as collateral for bills sold by a Japanese bank

subsidiary.

BH6/30 Adobe PageMaker 6.0J /PPC