Sony 2005 Annual Report Download - page 106

Download and view the complete annual report

Please find page 106 of the 2005 Sony annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

Sony Corporation 103

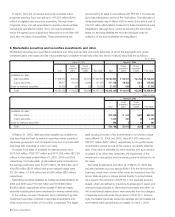

15. Pension and severance plans

Upon terminating employment, employees of Sony Corporation

and its subsidiaries in Japan are entitled, under most circum-

stances, to lump-sum indemnities or pension payments as

described below. For employees voluntarily retiring, payments

are determined based on current rates of pay and lengths of

service. In calculating the payments for employees involuntarily

retiring, including employees retiring due to meeting mandatory

retirement age requirements, Sony may grant additional benefits.

In July, 2004, Sony Corporation and certain of its subsidiaries

amended their pension plans and introduced a point-based plan

under which a point is added every year reflecting the individual

employee’s performance over that year. Under the point-based

plan the amount of payment is determined based on sum of

cumulative points from past services and interest points earned

on the cumulative points regardless of whether or not the em-

ployee is voluntarily retiring. As a result of the plan amendment,

the projected benefit obligation was decreased by ¥120,873

million ($1,130 million).

Sony Corporation and most of its subsidiaries in Japan have

contributory funded defined benefit pension plans, which are

pursuant to the Japanese Welfare Pension Insurance Law. The

contributory pension plans cover a substitutional portion of the

governmental welfare pension program, under which the contri-

butions are made by the companies and their employees, and

an additional portion representing the substituted noncontribu-

tory pension plans. Under the contributory pension plans, the

defined benefits representing the noncontributory portion of the

plans, in general, cover 65% of the indemnities under existing

regulations to employees. The remaining indemnities are cov-

ered by severance payments by the companies. The pension

benefits are payable at the option of the retiring employee either

in a lump-sum amount or monthly pension payments. Contribu-

tions to the plans are funded through several financial institutions

in accordance with the applicable laws and regulations.

In June 2001, the Japanese Government issued the Defined

Benefit Corporate Pension Plan Act which permits each

employer and employees’ pension fund plan to separate the

substitutional portion from its employees’ pension fund and

transfer the obligation and related assets to the government. In

July, 2004, in accordance with the law, the Japanese Govern-

ment approved applications submitted by Sony Corporation and

most of its subsidiaries in Japan for an exemption from the

obligation to pay benefits for future employee services related

to the substitutional portion of the governmental welfare pension

program. In January 2005, the government also approved

applications for an exemption from the obligation to pay benefits

for past employee services related to the substitutional portion.

As of March 31, 2005 the benefit obligation for past employee

services related to the substitutional portion and the related

government-specified portion of the plan assets have not been

transferred to the government.

EITF Issue No. 03-2, “Accounting for the Transfer to the

Japanese Government of the Substitutional Portion of Employee

Pension Fund Liabilities”, requires employers to account for the

entire separation process of a substitutional portion from an

entire plan upon completion of the transfer of the substitutional

portion of the benefit obligation and related plan assets to the

government as the culmination of a series of steps in a single

settlement transaction. In accordance with EITF Issue No. 03-2,

no accounting for the transfer was recorded for the year ended

March 31, 2005.

Many of foreign subsidiaries have defined benefit pension

plans or severance indemnity plans, which substantially cover all

of their employees. Under such plans, the related cost of ben-

efits is currently funded or accrued. Benefits awarded under

these plans are based primarily on the current rate of pay and

length of service.

Sony uses a measurement date of March 31 for substantially

all of its pension and severance plans.

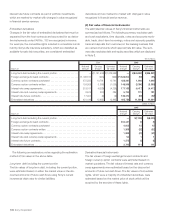

The components of net pension and severance costs, which

exclude employee termination benefits paid in restructuring

activities, for the years ended March 31, 2003, 2004 and 2005

were as follows:

Japanese plans:

Dollars in

Yen in millions millions

Years ended March 31 2003 2004 2005 2005

Service cost . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

¥(47,884 ¥(54,501 ¥(31,971 $(299

Interest cost . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

20,857 19,489 21,364 200

Expected return on plan assets . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(25,726) (22,812) (16,120) (151)

Amortization of net transition asset . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(375) (375) (375) (4)

Recognized actuarial loss . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

20,655 31,019 20,236 189

Amortization of prior service cost . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(939) (939) (7,216) (67)

Gains on curtailments and settlements . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

(1,380) — (876) (8)

Net periodic benefit cost . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .

¥(60,976 ¥(80,883 ¥(48,984 $(458

BH6/30 Adobe PageMaker 6.0J /PPC