Sony 2005 Annual Report Download - page 68

Download and view the complete annual report

Please find page 68 of the 2005 Sony annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

Sony Corporation 65

on high-quality fixed-income investments currently available and

expected to be available during the period to maturity of the

pension benefit obligation. The 2.3% discount rate represents a

10 basis point decrease from the 2.4% discount rate used for

fiscal year ended March 31, 2004 and reflects current market

interest rate conditions. For Japanese pension plans, a 10 basis

point decrease in the discount rate would increase pension

costs by approximately 1.2 billion yen for the fiscal year ending

March 31, 2006.

To determine the expected long-term rate of return on

pension plan assets, Sony considers the current and expected

asset allocations, as well as historical and expected long-term

rates of return on various categories of plan assets. For Japa-

nese pension plans, the expected long-term rate of return on

pension plan assets was 4.0% and 3.2% as of March 31, 2004

and 2005 respectively. The actual loss on pension plan assets

for the fiscal year ended March 31, 2005 was 0.1%. Actual

results that differ from the expected return on plan assets are

accumulated and amortized as a component of pension costs

over the average future service period, thereby reducing the

year-to-year volatility in pension costs. As of March 31, 2004

and 2005, Sony had unrecognized actuarial losses of 328.5

billion yen and 322.2 billion yen, respectively, including losses

related to plan assets. The unrecognized actuarial losses reflect

the overall unfavorable performance of equity markets over the

past several years and will result in an increase in pension costs

as they are recognized.

Sony recorded a liability for the unfunded accumulated benefit

obligation for Japanese pension plans of 149.4 billion yen and

128.6 billion yen as of March 31, 2004 and 2005, respectively.

This liability represents the excess of the accumulated benefit

obligation under Sony’s qualified defined benefit pension plans

over the fair value of the plans’ assets. This liability was estab-

lished by a charge to stockholders’ equity, resulting in no impact

to the accompanying consolidated statements of income.

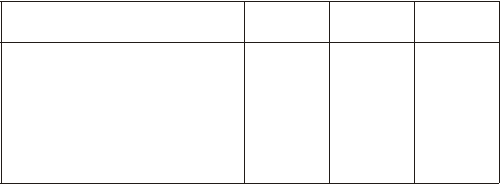

The following table illustrates the sensitivity to a change in the

discount rate and the expected return on pension plan assets,

while holding all other assumptions constant, for Japanese

pension plans as of March 31, 2005:

CHANGE IN ASSUMPTION

Yen in billions

Pre-tax Pension Equity

PBO expense (net of tax)

25 basis point increase /

decrease in discount rate . . . –/+45.0 –/+3.0 +/–1.8

25 basis point increase /

decrease in expected

return on assets . . . . . . . . . . — –/+1.3 +/–0.8

■DEFERRED TAX ASSET VALUATION

Sony records a valuation allowance to reduce the deferred tax

assets to an amount that management believes is more likely than

not to be realized. In establishing the appropriate valuation allow-

ance for deferred tax assets (including deferred tax assets on tax

loss carry-forwards), all available evidence, both positive and

negative, is considered. Information on historical results is supple-

mented by all currently available information on future years,

because realization of deferred tax assets is dependent on

whether each tax-filing unit generates sufficient taxable income.

The estimates and assumptions used in determining future

taxable income are consistent with those used in Sony’s approved

forecasts of future operations. Although realization is not assured,

management believes it is more likely than not that all of the

deferred tax assets, less valuation allowance, will be realized.

Sony applied to file its corporate income tax return under the

consolidated tax filing system in Japan beginning with the fiscal

year ended March 31, 2004. Under the consolidated tax filing

system, the tax-filing unit consists of Sony Corporation, the

ultimate parent company of the Sony Group, and its wholly

owned Japanese subsidiaries. The eventual ability to realize the

tax benefit of its deferred tax assets is dependent on whether

the tax-filing unit as a whole will be able to generate sufficient

taxable income in the future. In addition, Sony is subject to local

income taxes in Japan. For purposes of local income taxes,

each entity is taxed as a stand alone tax filing unit. The eventual

ability to realize the tax benefit of deferred tax assets for local

income taxes is dependent on whether Sony Corporation and

each subsidiary will be able to generate sufficient taxable

income in the future. As of March 31, 2005, Sony Corporation

had deferred tax assets for local income taxes totaling 77.5

billion yen. The eventual ability to realize the tax benefit of its

deferred tax assets is dependent on whether Sony Corporation

will be able to generate sufficient taxable income in the future.

Management believes that Sony Corporation’s historical results,

when evaluated in connection with relevant qualitative factors

and available information concerning its business and industry,

provided substantial positive evidence, which outweighs the

negative evidence available. However, under recent conditions,

management considers that it is possible that Sony

Corporation’s future results may yield sufficient negative evi-

dence to support the future determination that it is more likely

than not that Sony Corporation will not realize the tax benefit of

all these deferred tax assets. If this is the case, subject to review

of relevant qualitative factors and uncertainties, Sony may

establish a valuation allowance against part or all of the deferred

tax assets of Sony Corporation. Such valuation allowances

would be charged to income as an increase in tax expense.

BH6/30 Adobe PageMaker 6.0J /PPC