Sony 2005 Annual Report Download - page 88

Download and view the complete annual report

Please find page 88 of the 2005 Sony annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

Sony Corporation 85

■ Employers’ disclosures about pensions and other

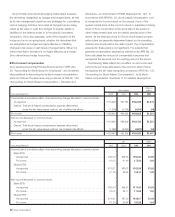

postretirement benefits

In December 2003, the Financial Accounting Standards Board

(“FASB”) issued FAS No. 132 (revised 2003), “Employers’ Disclo-

sures about Pensions and Other Postretirement Benefits” (“FAS

No. 132(R)”), which revised FAS No. 132, “Employers’ Disclosures

about Pensions and Other Postretirement Benefits”, an amend-

ment of FAS No. 87, “Employers’ Accounting for Pensions”, FAS

No. 88, “Employers’ Accounting for Settlements and Curtailments

of Defined Benefit Pension Plans and for Termination Benefits”,

and FAS No. 106, “Employers’ Accounting for Postretirement

Benefits Other Than Pensions”. FAS No. 132(R) revised employ-

ers’ disclosures about pension plans and other postretirement

benefit plans. It did not change the measurement or recognition of

those plans required by FAS No. 87, 88 and 106. While retaining

the disclosure requirements of FAS No. 132, FAS No. 132(R)

requires additional disclosures about assets, obligations and cash

flows. The provisions of FAS No. 132(R) were generally effective

for financial statements with fiscal years ending after December

15, 2003, excluding the disclosure of certain information about

foreign plans. The information about foreign plans is effective for

fiscal years ending after June 15, 2004. In accordance with FAS

No. 132(R), (Note 15), Pension and severance plans, has been

expanded to include the new disclosures.

■ Consolidation of variable interest entities

In January 2003, the FASB issued FASB Interpretation (“FIN”)

No. 46, “Consolidation of Variable Interest Entities—an Interpre-

tation of ARB No. 51”. FIN No. 46 addresses consolidation by a

primary beneficiary of a variable interest entity (“VIE”). Sony early

adopted the provisions of FIN No. 46 on July 1, 2003. As a

result of adopting the original FIN No. 46, Sony recognized a

one-time charge with no tax effect of ¥2,117 million as a cumu-

lative effect of accounting change in the consolidated statement

of income, and Sony’s assets and liabilities increased by

¥95,255 million and ¥97,950 million, respectively. These in-

creases were treated as non-cash transactions in the consoli-

dated statement of cash flows. In addition, cash and cash

equivalents increased by ¥1,521 million. See Note 23 for further

discussion on the VIEs that are used by Sony.

In December 2003, the FASB issued revised FIN No. 46 (“FIN

No. 46R”), which replaced FIN No. 46. Sony early adopted the

provisions of FIN No. 46R upon its issuance. The adoption of

FIN No. 46R did not have an impact on Sony’s results of opera-

tions and financial position or impact the way Sony had previ-

ously accounted for VIEs.

(2) Significant accounting policies:

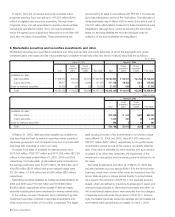

■ Basis of consolidation and accounting for investments in

affiliated companies

The consolidated financial statements include the accounts of

Sony Corporation and its majority-owned subsidiary companies,

general partnerships in which Sony has a controlling interest,

and variable interest entities for which Sony is the primary

beneficiary. All intercompany transactions and accounts are

eliminated. Investments in business entities in which Sony does

not have control, but has the ability to exercise significant influ-

ence over operating and financial policies generally through 20-

50% ownership, are accounted for under the equity method. In

addition, investments in general partnerships in which Sony

does not have a controlling interest and limited partnerships are

also accounted for under the equity method. Under the equity

method, investments are stated at cost plus/minus Sony’s

equity in undistributed earnings or losses. Consolidated net

income includes Sony’s equity in current earnings or losses of

such companies, after elimination of unrealized intercompany

profits. If the value of an investment has declined and is judged

to be other than temporary, the investment is written down to its

fair value.

On occasion, a consolidated subsidiary or an affiliated com-

pany accounted for by the equity method may issue its shares

to third parties in either a public or private offering or upon

conversion of convertible debt to common stock at amounts per

share in excess of or less than Sony’s average per share carry-

ing value. With respect to such transactions, where the sale of

such shares is not part of a broader corporate reorganization

and the reacquisition of such shares is not contemplated at the

time of issuance, the resulting gains or losses arising from the

change in interest are recorded in income for the year the

change in interest transaction occurs. If the sale of such shares

is part of a broader corporate reorganization, the reacquisition of

such shares is contemplated at the time of issuance or realiza-

tion of such gain is not reasonably assured (i.e., the entity is

newly formed, non-operating, a research and development or

start-up/development stage entity, or where the entity’s ability to

continue in existence is in question), the transaction is ac-

counted for as a capital transaction.

The excess of the cost over the underlying net equity of

investments in consolidated subsidiaries and affiliated compa-

nies accounted for on an equity basis is allocated to identifiable

assets and liabilities based on fair values at the date of acquisi-

tion. The unassigned residual value of the excess of the cost

over the underlying net equity is recognized as goodwill.

■ Use of estimates

The preparation of the consolidated financial statements in

conformity with U.S. GAAP requires management to make

estimates and assumptions that affect the reported amounts of

assets and liabilities and disclosure of contingent assets and

liabilities at the date of the financial statements and the reported

amounts of revenues and expenses during the reporting period.

Actual results could differ from those estimates.

BH6/30 Adobe PageMaker 6.0J /PPC