Sysco 2011 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2011 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

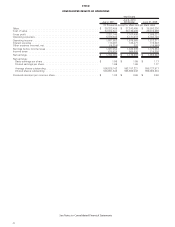

|

|

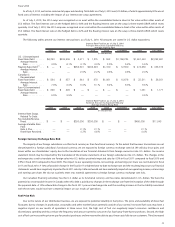

Fiscal 2010

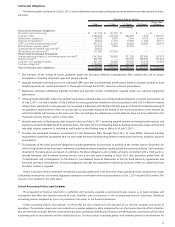

As of July 3, 2010, we had no commercial paper outstanding. Total debt as of July 3, 2010 was $2.5 billion, of which approximately 81% was at

fixed rates of interest including the impact of our interest rate swap agreements.

As of July 3, 2010, the 2014 swap was recognized as an asset within the consolidated balance sheet at fair value within other assets of

$5.5 million. The fixed interest rate on the hedged debt is 4.6% and the floating interest rate on the swap is three-month LIBOR which resets

quarterly. As of July 3, 2010, the 2013 swap was recognized as an asset within the consolidated balance sheet at fair value within other assets of

$5.5 million. The fixed interest rate on the hedged debt is 4.2% and the floating interest rate on the swap is three-month LIBOR which resets

quarterly.

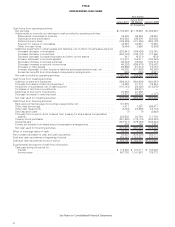

The following tables present our interest rate positions as of July 3, 2010. All amounts are stated in U.S. dollar equivalents.

2011 2012 2013 2014 2015 Thereafter Total Fair Value

Interest Rate Position as of July 3, 2010

Principal Amount by Expected Maturity

Average Interest Rate

(In thousands)

U.S. $ Denominated:

Fixed Rate Debt ...... $6,250 $204,658 $ 2,471 $ 1,275 $ 552 $1,766,234 $1,981,440 $2,262,961

Average Interest

Rate............ 4.5% 6.1% 4.7% 4.0% 3.5% 5.8% 5.9%

Floating Rate Debt

(1)

... $ — $ — $252,801 $208,249 $1,100 $ 12,500 $ 474,650 $ 483,872

Average Interest

Rate............ — — 2.5% 2.2% 0.3% 0.6% 2.3%

Canadian $

Denominated:

Fixed Rate Debt ...... $ 894 $ 957 $ 944 $ 979 $1,061 $ 18,676 $ 23,511 $ 26,851

Average Interest

Rate............ 7.6% 8.0% 8.8% 9.1% 9.2% 9.8% 9.5%

Euro eDenominated:

Fixed Rate Debt ...... $ 826 $ 205 $ — $ — $ — $ — $ 1,031 $ 1,177

Average Interest

Rate............ 8.9% 8.9% — — — — 8.9%

2011 2012 2013 2014 2015 Thereafter Total Fair Value

Interest Rate Position as of July 3, 2010

Notional Amount by Expected Maturity

Average Interest Swap Rate

(In thousands)

Interest Rate Swaps

Related To Debt:

Pay Variable/Receive

Fixed ............. $ — $ — $250,000 $200,000 $ — $ — $450,000 $11,045

Average Variable Rate

Paid:

Rate A Plus . ....... — — 2.1% 2.1% — — 2.1%

Fixed Rate Received . . — — 4.2% 4.6% — — 4.4%

Foreign Currency Exchange Rate Risk

The majority of our foreign subsidiaries use their local currency as their functional currency. To the extent that business transactions are not

denominated in a foreign subsidiary’s functional currency, we are exposed to foreign currency exchange rate risk. We will also incur gains and

losses within our shareholders’ equity due to the translation of our financial statements from foreign currencies into U.S. dollars. Our income

statement trends may be impacted by the translation of the income statements of our foreign subsidiaries into U.S. dollars. The changes in the

exchange rates used to translate our foreign sales into U.S. dollars positively impacted sales by 0.5% in fiscal 2011 compared to fiscal 2010 and

0.9% in fiscal 2010 compared to fiscal 2009. The impact to our operating income, net earnings and earnings per share was not material in fiscal

2011 and fiscal 2010. A 10% unfavorable change in the fiscal 2011 weighted year-to-date exchange rate and the resulting impact on our financial

statements would have negatively impacted fiscal 2011 sales by 0.6% and would not have materially impacted our operating income, net earnings

and earnings per share. We do not routinely enter into material agreements to hedge foreign currency exchange rate risks.

Our Canadian financing subsidiary has the U.S. dollar as its functional currency and has notes denominated in U.S. dollars. We have the

potential to create taxable income in Canada when this debt is paid due to changes in the exchange rate from the inception of the debt through

the payment date. A 10% unfavorable change in the fiscal 2011 year-end exchange rate and the resulting increase in the tax liability associated

with these notes would not have a material impact on our results of operations.

Fuel Price Risk

Due to the nature of our distribution business, we are exposed to potential volatility in fuel prices. The price and availability of diesel fuel

fluctuates due to changes in production, seasonality and other market factors generally outside of our control. Increased fuel costs may have a

negative impact on our results of operations in three areas. First, the high cost of fuel can negatively impact consumer confidence and

discretionary spending and thus reduce the frequency and amount spent by consumers for food-away-from-home purchases. Second, the high

cost of fuel can increase the price we pay for product purchases and we may not be able to pass these costs fully to our customers. Third, increased

35