Sysco 2011 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2011 Sysco annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

|

|

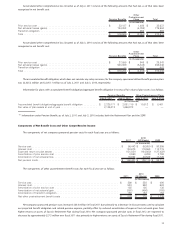

Subsequent Events

In February 2010, the FASB issued Accounting Standard Update 2010-09, “Amendments to Certain Recognition and Disclosure Require-

ments.” This update amends ASC 855, “Subsequent Events” to remove the requirement for SEC filers to disclose the date through which

subsequent events have been evaluated. In addition, the update clarifies the reissuance disclosure provision related to subsequent events. The

update is effective immediately for financial statements that are issued or revised. The company adopted the provisions of this update in the third

quarter of fiscal 2010. Because this update affects the disclosure and not the accounting treatment for subsequent events, the adoption of this

provision did not have a material impact on the company’s consolidated financial statements.

Employers’ Disclosures about Postretirement Benefit Plan Assets

In December 2008, the FASB issued FASB Staff Position No. FAS 132(R)-1, “Employers’ Disclosures about Postretirement Benefit Plan Assets”,

which was subsequently codified within ASC 715, “Compensation — Retirement Benefits”. This standard requires additional disclosures about

assets held in an employer’s defined benefit pension or other postretirement plan and became effective for Sysco in fiscal 2010. Sysco has

provided the required disclosures for this standard in Note 12, “Employee Benefit Plans.”

3. NEW ACCOUNTING STANDARDS

Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements in U.S. GAAP and IFRSs

In May 2011, the FASB issued Accounting Standard Update 2011-04, “Amendments to Achieve Common Fair Value Measurement and

Disclosure Requirements in U.S. GAAP and IFRSs.” This update amends ASC 820, “Fair Value Measurement” to improve the comparability of fair

value measurements presented and disclosed in financial statements prepared in accordance with U.S. GAAP and IFRSs. In addition, the update

explains how to measure fair value, but does not require additional fair value measurements and is not intended to establish valuation standards

or affect valuation practices outside of financial reporting. This update is effective for interim reporting periods ending after December 15, 2011,

which is the third quarter of fiscal 2012 for Sysco. The amendments in this update are to be applied prospectively and early application of this

standard is not permitted. Sysco is currently evaluating the impact the adoption of ASU 2011-04 will have on its consolidated financial statements.

Presentation of Comprehensive Income

In June 2011, the FASB issued Accounting Standard Update 2011-05, “Presentation of Comprehensive Income.” This update amends ASC 220,

“Comprehensive Income” to eliminate the option to present components of other comprehensive income as part of the statement of changes in

stockholders’ equity. The amendments require that all nonowner changes in stockholders’ equity be presented either in a single continuous

statement of comprehensive income or in two separate but consecutive statements. The amendments in this update do not change the items that

must be reported in other comprehensive income or when an item of other comprehensive income must be reclassified to net income. The

amendments in this update are effective for fiscal years, and interim periods within those years, beginning after December 15, 2011, which will be

fiscal 2013 for Sysco. The amendments in this update should be applied retrospectively and early application is permitted. Sysco is currently

evaluating which presentation option it will utilize for comprehensive income in its consolidated financial statements.

4. FAIR VALUE MEASUREMENTS

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market

participants at the measurement date (i.e. an exit price). The accounting guidance includes a fair value hierarchy that prioritizes the inputs to

valuation techniques used to measure fair value. The three levels of the fair value hierarchy are as follows:

•Level 1 — Unadjusted quoted prices for identical assets or liabilities in active markets;

•Level 2 — Inputs other than quoted prices in active markets for identical assets and liabilities that are observable either directly or

indirectly for substantially the full term of the asset or liability; and

•Level 3 — Unobservable inputs for the asset or liability, which include management’s own assumption about the assumptions market

participants would use in pricing the asset or liability, including assumptions about risk.

Sysco’s policy is to invest in only high-quality investments. Cash equivalents primarily include time deposits, certificates of deposit,

commercial paper, high-quality money market funds and all highly liquid instruments with original maturities of three months or less. Short-term

investments consist of commercial paper with original maturities of greater than three months but less than one year. These investments are

considered available-for-sale and are recorded at fair value. As of July 3, 2010, the difference between the fair value of the short-term investments

and the original cost was not material. There were no short-term investments as of July 2, 2011. Restricted cash consists of investments in high-

quality money market funds.

The following is a description of the valuation methodologies used for assets and liabilities measured at fair value.

• Time deposits, certificates of deposit and commercial paper included in cash equivalents are valued at amortized cost, which

approximates fair value. These are included within cash equivalents as a Level 2 measurement in the tables below.

49