Cabela's 2009 Annual Report Download - page 100

Download and view the complete annual report

Please find page 100 of the 2009 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

91

CABELA’S INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in Thousands Except Share and Per Share Amounts)

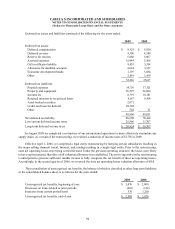

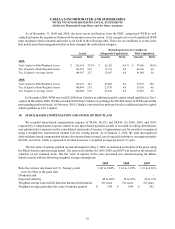

WFB has unsecured federal funds purchase agreements with two financial institutions. The maximum amount that can

be borrowed is $85,000. There were no amounts outstanding at the end of December 2009 or 2008. During 2009 and 2008,

the average balance outstanding was $151 and $25,790 with a weighted average rate of 0.22% and 2.90%, respectively.

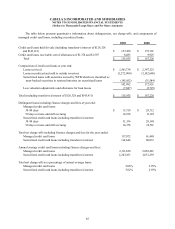

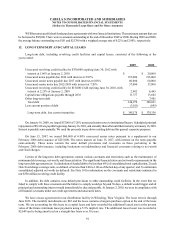

12. LONG-TERM DEBT AND CAPITAL LEASES

Long-term debt, including revolving credit facilities and capital leases, consisted of the following at the

years ended:

2009 2008

Unsecured revolving credit facility for $350,000 expiring June 30, 2012 with

interest at 1.96% at January 2, 2010 $ - $ 20,000

Unsecured notes payable due 2016 with interest at 5.99% 215,000 215,000

Unsecured senior notes payable due 2017 with interest at 6.08% 60,000 60,000

Unsecured senior notes due 2012-2018 with interest at 7.20% 57,000 57,000

Unsecured revolving credit facility for $15,000 CAD expiring June 30, 2010, with

interest at 2.25% at January 2, 2010 2,902 6,465

Capital lease obligations payable through 2036 13,377 13,665

Other long-term debt - 7,901

Total debt 348,279 380,031

Less current portion of debt (3,101)(695)

Long-term debt, less current maturities $ 345,178 $379,336

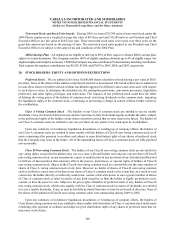

On January 16, 2008, we issued $57,000 of 7.20% unsecured senior notes to institutional buyers. Scheduled principal

repayments of $8,143 are payable beginning January 16, 2012, and annually thereafter until their maturity at January 16, 2018.

Interest is payable semi-annually. We used the proceeds to pay down existing debt and for general corporate purposes.

On June 15, 2007, we issued $60,000 of 6.08% unsecured senior notes pursuant to a supplement to our

February 2006 debt issuance of $215,000. The notes mature on June 15, 2017, with interest on the notes payable

semi-annually. These notes contain the same default provisions and covenants as those pertaining to the

February 2006 debt issuance, including limitations on indebtedness and financial covenants relating to net worth

and fixed charges.

Certain of the long-term debt agreements contain various covenants and restrictions such as the maintenance of

minimum debt coverage, net worth, and financial ratios. The significant financial ratios and net worth requirements in the

long-term debt agreements are 1) a limitation of funded debt to be less than 60% of consolidated total capitalization; 2) cash

flow fixed charge coverage ratio, as defined, of no less than 2.00 to 1.00 as of the last day of any quarter; and 3) a minimum

consolidated adjusted net worth (as defined). See Note 10 for information on the covenants and restrictions contained in

our $350 million revolving credit facility.

In addition, the debt contains cross default provisions to other outstanding credit facilities. In the event that we

failed to comply with these covenants and the failure to comply would go beyond 30 days, a default would trigger and all

principal and outstanding interest would immediately be due and payable. At January 2, 2010, we were in compliance with

all financial covenants under our credit agreements and unsecured notes.

We have a lease agreement for our distribution facility in Wheeling, West Virginia. The lease term is through

June 2036. The monthly installments are $83 and the lease contains a bargain purchase option at the end of the lease

term. We are accounting for this lease as a capital lease and have recorded the additional leased asset at the present

value of the future minimum lease payments using a 5.9% implicit rate. The additional leased asset was recorded at

$5,649 and is being amortized on a straight-line basis over 30 years.