Cabela's 2009 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2009 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

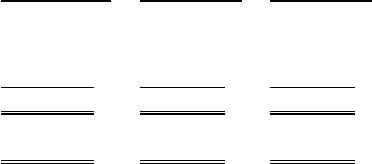

52

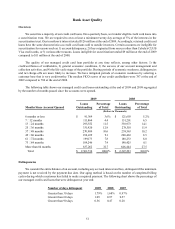

Charge-offs

Charge-offs consist of the uncollectible principal, interest, and fees on a customer’s account. Recoveries are the

amounts collected on previously charged-off accounts. Most bankcard issuers charge-off accounts at 180 days. We

charge off credit card loans on a daily basis after an account becomes at a minimum 130 days contractually delinquent

to allow us to manage the collection process more efficiently. Accounts relating to cardholder bankruptcies, cardholder

deaths, and fraudulent transactions are charged off earlier. Our charge-off activity for the managed portfolio is

summarized below for the years ended:

2009 2008 2007

(Dollars in Thousands)

Charge-offs $127,539 $70,944 $42,853

Recoveries (10,467)(9,496)(8,955)

Net charge-offs $ 117,072 $61,448 $33,898

Net charge-offs as a percentage of average

managed credit card loans 5.06%2.95%2.01%

For 2009, net charge-offs as a percentage of average managed credit card loans increased to 5.06%, up 211 basis

points compared to 2.95% for 2008, principally because of the challenging economic environment. We believe our

charge-off levels remain below industry average.

Liquidity and Capital Resources

Overview

We believe that we will have sufficient capital available from cash on hand, our revolving credit facility, and

other borrowing sources to fund our foreseeable cash requirements and near-term growth plans. At the end of 2009

and 2008, cash on a consolidated basis totaled $582 million and $410 million, respectively, of which $371 million and

$402 million, respectively, was cash at our Financial Services business segment which will be utilized to meet this

segment’s liquidity requirements. In 2009, our Financial Services business completed a term securitization totaling

$500 million, renewed and increased a $214 million variable funding facility to $260 million, and renewed and

increased a $376 million variable funding facility to $412 million. We will continue to evaluate additional funding

sources to determine the most cost effective source of funds for our Financial Services business segment. These

potential sources include, among others, certificates of deposit and securitizations.

Our Retail and Direct business segments and our Financial Services business segment have significantly

differing liquidity and capital needs. The primary cash requirements of our merchandising business relate to capital

for new retail stores, purchases of inventory, investments in our management information systems and infrastructure,

purchases of economic development bonds related to the construction of new retail stores, and general working capital

needs. We historically have met these requirements with cash generated from our merchandising business operations,

borrowing under revolving credit facilities, issuing debt and equity securities, obtaining economic development

grants from state and local governments in connection with developing our retail stores, collecting principal and

interest payments on our economic development bonds, and from the retirement of economic development bonds.

Retail and Direct Business Segments – The cash flow we generate from our merchandising business is

seasonal, with our peak cash requirements for inventory occurring from April through November. While we have

consistently generated overall positive annual cash flow from our operating activities, other sources of liquidity are

required by our merchandising business during these peak cash use periods. These sources historically have included

short-term borrowings under our revolving credit facility and access to debt markets. While we generally have been