Cabela's 2009 Annual Report Download - page 92

Download and view the complete annual report

Please find page 92 of the 2009 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

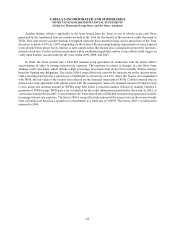

83

CABELA’S INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in Thousands Except Share and Per Share Amounts)

including asset-backed securities.” Each class of notes issued in the securitization transaction has an expected life

of approximately three years, with a contractual maturity of approximately six years. This securitization transaction

refinanced asset-backed notes issued by the Trust that matured in 2009.

On April 4, 2009, WFB purchased triple-A rated notes with a par value of $2,100 at a discount in the secondary

markets from previously issued series of the Trust. These notes are classified as asset-backed available-for-sale

securities and classified in the consolidated balance sheet under the caption “retained interests in securitized loans,

including asset-backed securities.”

On June 5, 2009, the Trust renewed and increased a $213,904 variable funding facility to a $260,115 variable

funding facility that will mature in June 2010. In addition, on September 15, 2009, the Trust renewed and increased a

$376,355 variable funding facility to a $411,765 variable funding facility that will mature in September 2010.

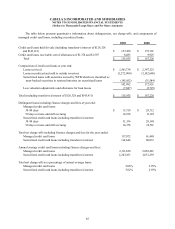

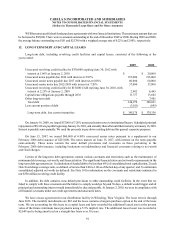

WFB’s retained interest, including asset-backed securities, and related receivables are comprised of the

following at the end of:

2009 2008

Asset-backed trading securities $ 68,752 $31,584

Asset-backed available for sale securities (amortized cost of $76,984) 82,705 -

Interest-only strip, cash reserve accounts, and cash accounts 24,577 30,021

Transferor’s interest 126,328 143,411

Other assets - accrued interest receivable and amounts due from the Trust 38,278 32,379

Total $ 340,640 $237,395

WFB’s retained interests are subject to credit, payment, and interest rate risks on the transferred credit card

receivables. To protect investors, the securitization structures include certain features that could result in earlier-

than-expected repayment of the securities, which could cause WFB to sustain a loss of one or more of its retained

interests and could prompt the need for WFB to seek alternative sources of funding. The primary investor protection

feature relates to the availability and adequacy of cash flows in the securitized pool of receivables to meet contractual

requirements, the insufficiency of which triggers early repayment of the securities. WFB refers to this as the “early

amortization” feature. Investors are allocated cash flows derived from activities related to the accounts comprising

the securitized pool of receivables, the amounts of which reflect finance charges collected, certain fee assessments

collected, allocations of interchange, and recoveries on charged off accounts. From these cash flows, investors are

reimbursed for charge-offs occurring within the securitized pool of receivables and receive a contractual rate of return

and WFB is paid a servicing fee as servicer. Any cash flows remaining in excess of these requirements are paid to

WFB and recorded as excess spread, included in securitization income. An excess spread of less than zero percent for

a contractually specified period, generally a three-month average, would trigger an early amortization event. Once

the excess spread falls below zero percent, the receivables that would have been subsequently purchased by the Trust

from WFB will instead continue to be recognized on the consolidated balance sheet since the cash flows generated

in the Trust would be used to repay principal to investors. Such an event could result in WFB incurring losses related

to its retained interests, including amounts due from the Trust, investments in asset-backed securities, interest-only

strip receivables, cash reserve account, cash accounts and accrued interest receivable. The investors have no recourse

to WFB’s other assets for failure of debtors to pay other than for breaches of certain customary representations,

warranties, and covenants. These representations, warranties, covenants, and the related indemnities, do not protect

the Trust or the outside investors against credit-related losses on the loans.