Cabela's 2009 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2009 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

36

Full implementation of the CARD Act requires the promulgation of regulations by the Federal Reserve.

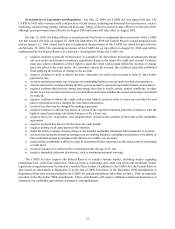

The Federal Reserve has issued final regulations implementing the majority of the provisions of the CARD Act.

WFB continues to evaluate the effects of the CARD Act and is making changes that the CARD Act requires to

be implemented in a relatively short timeframe. Other changes must await final regulatory guidance from the

Federal Reserve. WFB is continuing to evaluate appropriate modifications to its products, revenue generation,

marketing strategies, and other business practices that will be in compliance with the law. The full impact of

the CARD Act on WFB is unknown at this time as it ultimately depends upon continued regulatory actions

and successful implementation of WFB’s strategies. Compliance with the CARD Act provisions could result in

reduced interest income and other fee income. WFB issued changes in terms effective July 2009 to lessen the

effects of the CARD Act.

On June 17, 2009, the Obama administration released its white paper (the “White paper”) for proposed reform of

the financial system. Proposed reforms which could materially affect WFB include the elimination of the exemption

from the definition of “bank” under the Bank Holding Company Act of 1956, as amended (the “BHCA”) for credit

card banks, such as WFB and increased supervision and regulation of financial firms. Since the issuance of the White

Paper, different forms of legislation to implement the administration’s plan have been introduced in both houses of

the Congress. The bills, though different at present, address risks to the economy and the payments system, especially

those posed by large “systemically significant” financial firms, through a variety of measures, including regulatory

oversight of nonbanking entities, increased capital requirements, enhanced authority to limit activities and growth,

changes in supervisory authority, resolution authority for failed financial firms, enhanced regulation of derivatives

and asset-backed securities, restrictions on executive compensation, and oversight of credit rating agencies. Due to

the complexity and controversial nature of the proposed bills, modifications are likely and the final legislation, if

any, may differ significantly from the administration’s original proposal. Additionally, compliance with potential

increased regulation and scrutiny by multiple state and federal agencies may reduce WFB’s profitability, which could

negatively impact our business. It is unclear whether any enacted legislation will preserve, eliminate, or modify

the exemption for credit card banks under the BHCA. If such exemption were eliminated or modified, we may be

required to divest our ownership of WFB unless we were willing and able to become a bank holding company under

the BHCA. Any such forced divestiture would materially adversely affect our business and results of operation.

Impact of New Accounting Pronouncements – The guidance of Accounting Standards Codification (“ASC”)

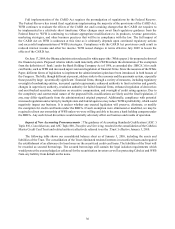

Topic 810, Consolidations, and ASC Topic 860, Transfers and Servicing, resulted in the consolidation of the Cabela’s

Master Credit Card Trust and related entities (collectively referred to as the “Trust”) effective January 3, 2010.

The following table shows our consolidated balance sheet as of January 3, 2010, including the assets and

liabilities of the Trust. The consolidation of the Trust eliminated retained interests in securitized loans and required

the establishment of an allowance for loan losses on the securitized credit card loans. The liabilities of the Trust will

be recorded as secured borrowings. The secured borrowings still contain the legal isolation requirements which

would protect the assets pledged as collateral for the securitization investors as well as protecting Cabela’s and WFB

from any liability from default on the notes.