Cabela's 2009 Annual Report Download - page 115

Download and view the complete annual report

Please find page 115 of the 2009 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

-

127

-

128

-

129

-

130

-

131

|

|

106

CABELA’S INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in Thousands Except Share and Per Share Amounts)

current market rates; indicative pricing for such instruments; the rates from the last date WFB considered the market

for these instruments to be active and orderly, adjusted for changes in credit spreads in accordance with ASC Section

820-10-35, Fair Value Measurements and Disclosures: Overall: Subsequent Measurement and ASC Section 820-10-

65, Fair Value Measurements and Disclosures: Overall: Transition and Open Effective Date Information; and the

discount rates used to value other retained interests in securitized loans. At the end of December 2009, the weighted

average discount rate used to value the triple-A rated notes was 1.34%, the A rated notes was 5.16%, the triple-B rated

notes was 6.56%, and the double-B rated notes was 11.00%. Declines in the fair value of asset-backed available for

sale securities below amortized cost that are deemed to be other than temporary are reflected in current earnings.

Fair values of economic development bonds (“bonds”) are estimated using discounted cash flow projection

estimates based on available market interest rates and the estimated amounts and timing of expected future payments

to be received from municipalities under tax development zones. These fair values do not reflect any premium or

discount that could result from offering these bonds for sale or through early redemption, or any related income tax

impact. Declines in the fair value of held-to-maturity and available-for-sale economic development bonds below cost

that are deemed to be other than temporary are reflected in earnings. During 2009, 2008, and 2007, we evaluated the

recovery of certain bonds and determined their fair value using significant unobservable inputs (Level 3) as defined

by and in accordance with the provisions of ASC Topic 820. The fair value of these bonds was determined to be below

carrying value, with the decline in fair value deemed to be other than temporary, resulting in fair value adjustments

totaling $8,032, $1,280, and $6,733 at the end of 2009, 2008, and 2007, respectively, reducing the carrying value of

the bond portfolio.

Certain assets are measured at fair value on a non-recurring basis using significant unobservable inputs

(Level 3) as defined by and in accordance with the provisions of ASC Topic 820. As such, property and equipment,

land held for sale, goodwill, and other intangibles with a net carrying amount totaling $136,572 were written down to

their fair value of $76,345 during 2009. These write-downs resulted in a total impairment charge of $60,227 reflected

in earnings for the year ended 2009.

The estimated fair value of credit card loans receivable and the credit card loans held for sale is based on the

present value of future expected cash flows using assumptions for credit losses, payment rates, finance charge yield,

and discount rates commensurate with the risks involved. This valuation does not include the value that relates to

estimated cash flows generated from new loans over the life of the cardholder relationship. Accordingly, the aggregate

fair value of the credit card loans does not represent the underlying value of the established cardholder relationship.

Time deposits are pooled in homogeneous groups and the future cash flows of these groups are discounted using

current market rates offered for similar products for estimating fair value.

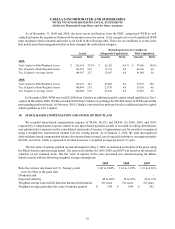

The following table provides the estimated fair values of financial instruments not carried at fair value at the

years ended:

2009 2008

Carrying

Value Estimated

Fair Value Carrying

Value Estimated

Fair Value

Financial Assets

Credit card loans, net $ 135,935 $140,199 $167,226 $168,429

Financial Liabilities

Time deposits 476,664 499,838 486,199 508,190

Long-term debt 348,279 343,108 380,031 373,304