Cabela's 2009 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2009 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

96

CABELA’S INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in Thousands Except Share and Per Share Amounts)

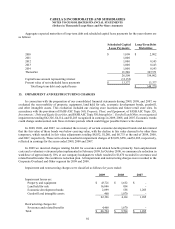

In April 2007, we began an open account document instructions program, which provides for our company-

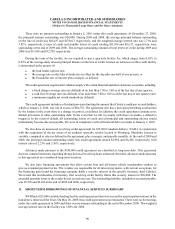

issued letters of credit. At the end of 2009 and 2008, we had obligations to pay participating vendors $23,471 and

$35,622, respectively.

WFB enters into financial instruments with off balance sheet risk in the normal course of business through the

origination of unsecured credit card loans. Unsecured credit card accounts are commitments to extend credit and

totaled $12,996,000 and $12,886,000 at January 2, 2010, and December 27, 2008, respectively. These commitments

are in addition to any current outstanding balances of a cardholder. Unsecured credit card loans involve, to varying

degrees, elements of credit risk in excess of the amount recognized in the consolidated balance sheets. The principal

amounts of these instruments reflect WFB’s maximum related exposure. WFB has not experienced and does not

anticipate that all customers will exercise the entire available line of credit at any given point in time. WFB has the

right to reduce or cancel the available lines of credit at any time.

Litigation and Claims – We are party to various proceedings, lawsuits, disputes, and claims arising in the

ordinary course of our business. These actions include commercial, intellectual property, employment, and product

liability claims. Some of these actions involve complex factual and legal issues and are subject to uncertainties. We

cannot predict with assurance the outcome of the actions brought against us. Accordingly, adverse developments,

settlements, or resolutions may occur and negatively impact earnings in the quarter of such development, settlement,

or resolution. However, we do not believe that the outcome of any current action would have a material adverse effect

on our results of operations, cash flows, or financial position taken as a whole.

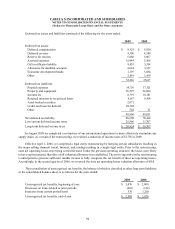

Self-Insurance – We are self-insured for health claims up to $300 per individual. We have established a liability

for health claims submitted and for those claims incurred prior to year end but not yet reported totaling $2,389 and

$3,445 at the end of 2009 and 2008, respectively.

We are also self-insured for workers’ compensation claims up to $500 per individual. We have established

a liability for workers’ compensation claims submitted and for those claims incurred prior to year end but not yet

reported totaling $3,874 and $4,198 at the end of 2009 and 2008, respectively.

Our liabilities for health and workers’ compensation claims incurred but not reported are based upon internally

developed calculations. These estimates are regularly evaluated for adequacy based on the most current information

available, including historical claim payments, expected trends, and industry factors.

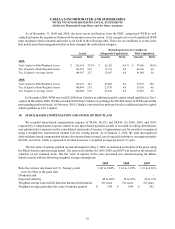

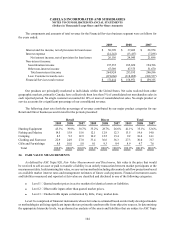

17. REGULATORY CAPITAL REQUIREMENTS

WFB is subject to various regulatory capital requirements administered by the FDIC and the Nebraska State

Department of Banking and Finance. Under capital adequacy guidelines and the regulatory framework for prompt

corrective action, WFB must meet specific capital guidelines that involve quantitative measures of WFB’s assets,

liabilities, and certain off-balance sheet items as calculated under regulatory accounting practices. WFB’s capital

amounts and classification are also subject to qualitative judgment by the regulators with respect to components, risk

weightings, and other factors.

The quantitative measures established by regulation to ensure capital adequacy require that WFB maintain

minimum amounts and ratios (defined in the regulations) as set forth in the following table. WFB exceeded the

minimum requirements for the well-capitalized category under the regulatory framework for prompt corrective

action for both periods presented.