Cabela's 2009 Annual Report Download - page 93

Download and view the complete annual report

Please find page 93 of the 2009 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

84

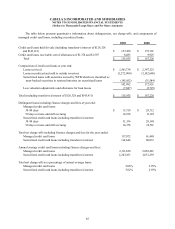

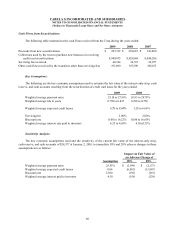

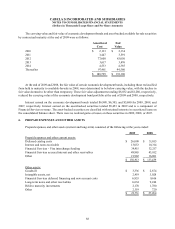

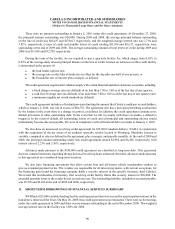

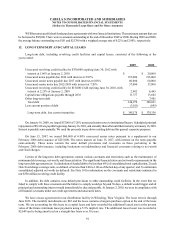

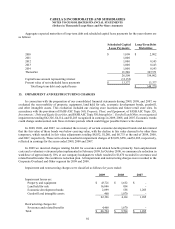

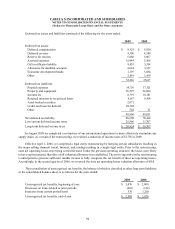

CABELA’S INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in Thousands Except Share and Per Share Amounts)

Another feature, which is applicable to the notes issued from the Trust, is one in which excess cash flows

generated by the transferred loan receivables are held at the Trust for the benefit of the investors, rather than paid to

WFB. This cash reserve account funding is triggered when the three-month average excess spread rate of the Trust

decreases to below 4.50% or 5.50% (depending on the series) with increasing funding requirements as excess spread

levels decline below preset levels. Similar to early amortization, this feature also is designed to protect the investors’

interests from loss. Credit card loans performed within established guidelines and no events which could trigger an

“early amortization” occurred during the years ended 2009, 2008, and 2007.

In 2008, the Trust entered into a $229,850 notional swap agreement in connection with the Series 2008-I

securitization in order to manage interest rate exposure. The exposure is related to changes in cash flows from

funding credit card loans, which include a high percentage of accounts that do not incur monthly finance charges

based on floating rate obligations. The Series 2008-I swap effectively converts the interest rate on the investor notes

from a floating rate based on a spread over a benchmark to a fixed rate of 4.32%. Since the Trust is not consolidated

with WFB, the fair value of the swap is not reflected on the financial statements of WFB. Cabela’s entered into an

interest rate swap agreement with similar terms with the counterparty where the notional amount of Cabela’s swap

is zero unless the notional amount of WFB’s swap falls below a required amount, effectively making Cabela’s a

guarantor of WFB’s swap. WFB pays a fee to Cabela’s for the credit enhancement provided by this swap. In 2003, in

connection with the Series 2003-1 securitization, the Trust entered into a $300,000 notional swap agreement in order

to manage interest rate exposure. The Series 2003-1 swap effectively converted the interest rate on the investor bonds

from a floating rate based on a spread over a benchmark to a fixed rate of 3.699%. The Series 2003-1 securitization

matured in 2008.