Cabela's 2009 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2009 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

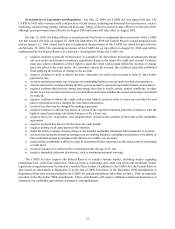

35

Developments in Legislation and Regulation – On May 22, 2009, the CARD Act was signed into law. The

CARD Act will affect various credit card practices of card issuers, including our Financial Services business, such as

marketing, underwriting, pricing, billing and disclosure. Many of the provisions became effective in February 2010,

although some provisions were effective in August 2009 and some will take effect in August 2010.

On July 15, 2009, the Federal Reserve issued interim final rules to implement those provisions of the CARD

Act that became effective on August 20, 2009. On September 29, 2009, the Federal Reserve issued proposed rules

and on January 12, 2010, issued final rules to implement the provisions of the CARD Act which became effective

on February 22, 2010. The remaining provisions of the CARD Act go into effect on August 22, 2010, and will be

implemented by the Federal Reserve at a later date. Among other things, the CARD Act:

• requires creditors to provide written notice to consumers 45 days before increasing an annual percentage

rate on a credit card account or making a significant change to the terms of a credit card account. Creditors

must also inform consumers of their right to cancel the credit card account before the increase or change

goes into effect in the same notice. If a consumer cancels the account, the creditor is generally prohibited

from applying the increase or change to the account.

• requires creditors to mail or deliver periodic statements for credit card accounts at least 21 days before

payment is due;

• restricts annual percentage rate increases on outstanding balances except under limited circumstances;

• restricts interest rate increases during the first year an account is opened except under limited circumstances;

• requires creditors that increase annual percentage rates due to credit criteria, market conditions, or other

factors to review accounts at least every six months to determine whether the annual percentage rate should

be reduced;

• requires creditors to obtain the credit card account holders opt-in in order to assess an over-limit fee and

places restrictions on fees charged for over-limit transactions;

• restricts fees that may be charged for making a payment;

• requires creditors to allocate payments in excess of the required minimum payment to balances with the

highest annual percentage rate before balances with a lower rate;

• requires fees to be “reasonable” and “proportionate” based on the violation of the terms of the cardholder

agreement;

• requires payment due dates to be the same day each month;

• requires posting of all agreements on the Internet;

• limits the ability to charge finance charge in the month a cardholder transitions from transactor to revolver;

• restricts increasing the annual percentage rate on existing balances, including restrictions on the ability to

have minimum annual percentage rates (floors) on variable rate accounts;

• requires that a cardholder’s ability to repay be determined before opening a credit card account or increasing

a credit limit;

• restricts issuance of a credit card to a consumer under the age of 21; and

• requires expanded statement disclosures, such as minimum payment warning.

The CARD Act also requires the Federal Reserve to conduct various studies, including studies regarding

interchange fees, credit limit reductions, financial literacy, marketing, and credit card terms and conditions. Future

legislation or regulations may be issued as a result of these studies. In addition to the CARD Act, the Federal Reserve

also issued an amendment to Regulation Z at the end of 2008. Provisions in the December 2008 amendments to

Regulation Z that were not superseded by the CARD Act remain scheduled to take effect on July 1, 2010, as originally

provided in the December 2008 amendments. These amendments will require additional enhanced disclosures to

consumers on cardholder agreements, statements, and applications.