Cabela's 2009 Annual Report Download - page 113

Download and view the complete annual report

Please find page 113 of the 2009 Cabela's annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

104

CABELA’S INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Dollars in Thousands Except Share and Per Share Amounts)

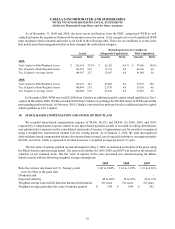

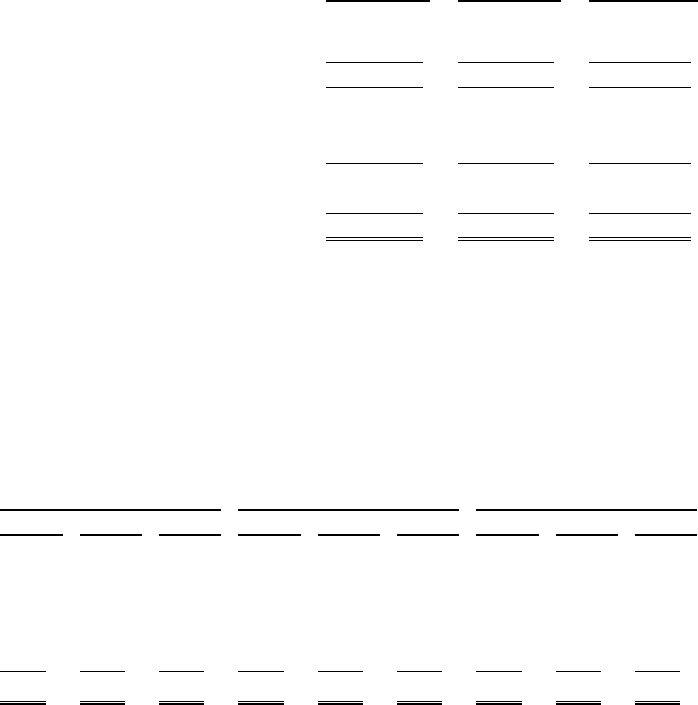

The components and amounts of total revenue for the Financial Services business segment were as follows for

the years ended:

2009 2008 2007

Interest and fee income, net of provision for loan losses $ 50,398 $37,462 $28,974

Interest expense (24,242)(13,417)(7,288)

Net interest income, net of provision for loan losses 26,156 24,045 21,686

Non-interest income:

Securitization income 197,335 185,820 194,516

Other non-interest income 67,589 67,375 51,670

Total non-interest income 264,924 253,195 246,186

Less: Customer rewards costs (119,666)(118,269)(108,537)

Financial Services total revenue $ 171,414 $158,971 $159,335

Our products are principally marketed to individuals within the United States. Net sales realized from other

geographic markets, primarily Canada, have collectively been less than 3% of consolidated net merchandise sales in

each reported period. No single customer accounted for 10% or more of consolidated net sales. No single product or

service accounts for a significant percentage of our consolidated revenue.

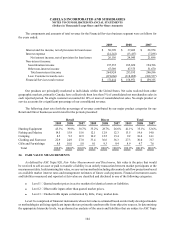

The following chart sets forth the percentage of revenue contributed by our major product categories for our

Retail and Direct businesses and in total for the periods presented:

Retail Direct Total

2009 2008 2007 2009 2008 2007 2009 2008 2007

Hunting Equipment 45.3%39.9%38.7%35.2%28.7%26.6%41.1%35.1%32.6%

Fishing and Marine 14.5 15.9 15.6 12.1 12.9 12.3 13.5 14.6 14.0

Camping 8.5 9.3 12.9 10.2 12.5 15.4 9.2 10.614.1

Clothing and Footwear 22.9 24.9 27.0 33.4 36.6 36.3 27.3 30.0 31.7

Gifts and Furnishings 8.8 10.0 5.8 9.19.3 9.4 8.9 9.7 7.6

Total 100.0%100.0%100.0%100.0%100.0%100.0%100.0%100.0%100.0%

24. FAIR VALUE MEASUREMENTS

As defined by ASC Topic 820, Fair Value Measurements and Disclosures, fair value is the price that would

be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the

measurement date. In determining fair value, we use various methods including discounted cash flow projections based

on available market interest rates and management estimates of future cash payments. Financial instrument assets

and liabilities measured and reported at fair value are classified and disclosed in one of the following categories:

• Level 1 – Quoted market prices in active markets for identical assets or liabilities.

• Level 2 – Observable inputs other than quoted market prices.

• Level 3 – Unobservable inputs corroborated by little, if any, market data.

Level 3 is comprised of financial instruments whose fair value is estimated based on internally developed models

or methodologies utilizing significant inputs that are primarily unobservable from objective sources. In determining

the appropriate hierarchy levels, we performed an analysis of the assets and liabilities that are subject to ASC Topic