Humana 2010 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2010 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

Humana Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

municipal securities were pre-refunded, generally with U.S. government and agency securities, and 25% of our

tax-exempt securities were insured by bond insurers and had an equivalent S&P credit rating of AA exclusive of

the bond insurers’ guarantee. Our investment policy limits investments in a single issuer and requires

diversification among various asset types.

The recoverability of our residential and commercial mortgage-backed securities is supported by factors

such as seniority, underlying collateral characteristics and credit enhancements. Our residential and commercial

mortgage-backed securities at December 31, 2010 primarily were composed of senior tranches having high credit

support, with 99% of the collateral consisting of prime loans. All commercial mortgage-backed securities were

rated AA+ at December 31, 2010.

All issuers of securities we own that were trading at an unrealized loss at December 31, 2010 remain current

on all contractual payments. After taking into account these and other factors previously described, we believe

these unrealized losses primarily were caused by an increase in market interest rates and tighter liquidity

conditions in the current markets than when the securities were purchased. At December 31, 2010, we did not

intend to sell the securities with an unrealized loss position in accumulated other comprehensive income, and it is

not likely that we will be required to sell these securities before recovery of their amortized cost basis. As a

result, we believe that the securities with an unrealized loss were not other-than-temporarily impaired at

December 31, 2010.

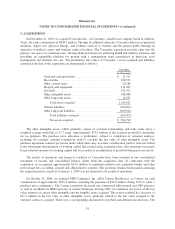

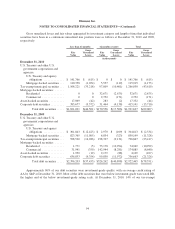

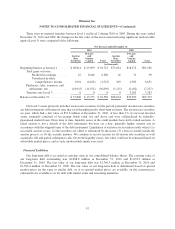

The detail of realized gains (losses) related to investment securities and included within investment income

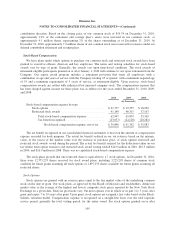

was as follows for the years ended December 31, 2010, 2009, and 2008:

2010 2009 2008

(in thousands)

Gross realized gains .......................... $34,815 $ 123,361 $ 56,879

Gross realized losses ......................... (29,169) (103,878) (136,296)

Net realized capital gains (losses) ........... $ 5,646 $ 19,483 $ (79,417)

There were no material other-than-temporary impairments in 2010 or 2009. Gross realized losses in 2008

included other-than-temporary impairments of $103.1 million, primarily due to investments in Lehman Brothers

Holdings Inc. and certain of its subsidiaries, which filed for bankruptcy protection in 2008, as well as declines in

the values of securities primarily associated with the financial services industry.

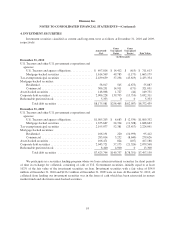

The contractual maturities of debt securities available for sale at December 31, 2010, regardless of their

balance sheet classification, are shown below. Expected maturities may differ from contractual maturities

because borrowers may have the right to call or prepay obligations with or without call or prepayment penalties.

Amortized

Cost

Fair

Value

(in thousands)

Due within one year .......................... $ 299,861 $ 301,630

Due after one year through five years ............. 1,936,215 1,991,966

Due after five years through ten years ............ 2,072,510 2,134,576

Due after ten years ............................ 1,740,450 1,754,419

Mortgage and asset-backed securities ............. 2,126,945 2,189,848

Total debt securities ...................... $8,175,981 $8,372,439

95