Humana 2010 Annual Report Download - page 82

Download and view the complete annual report

Please find page 82 of the 2010 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

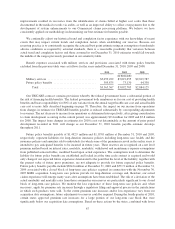

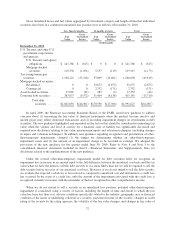

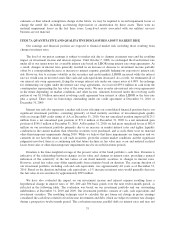

Gross unrealized losses and fair values aggregated by investment category and length of time that individual

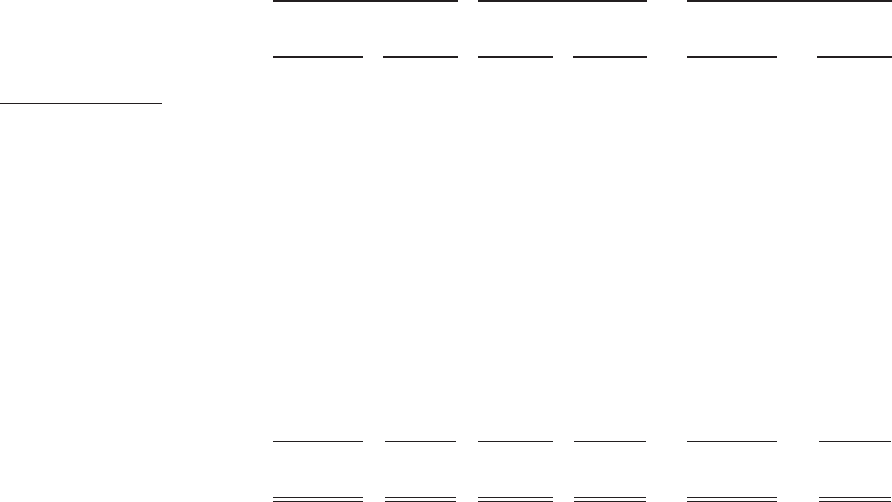

securities have been in a continuous unrealized loss position were as follows at December 31, 2010:

Less than 12 months 12 months or more Total

Fair

Value

Gross

Unrealized

Losses

Fair

Value

Gross

Unrealized

Losses

Fair

Value

Gross

Unrealized

Losses

(in thousands)

December 31, 2010

U.S. Treasury and other U.S.

government corporations

and agencies:

U.S. Treasury and agency

obligations .......... $ 141,766 $ (615) $ 0 $ 0 $ 141,766 $ (615)

Mortgage-backed

securities ........... 110,358 (1,054) 5,557 (119) 115,915 (1,173)

Tax-exempt municipal

securities ............... 1,168,221 (33,218) 97,809 (10,401) 1,266,030 (43,619)

Mortgage-backed securities:

Residential ............ 0 0 32,671 (2,675) 32,671 (2,675)

Commercial ........... 0 0 2,752 (171) 2,752 (171)

Asset-backed securities ...... 17,069 (42) 283 (2) 17,352 (44)

Corporate debt securities ..... 383,677 (9,572) 31,464 (4,138) 415,141 (13,710)

Total debt

securities ....... $1,821,091 $(44,501) $170,536 $(17,506) $1,991,627 $(62,007)

In April 2009, the Financial Accounting Standards Board, or the FASB, issued new guidance to address

concerns about (1) measuring the fair value of financial instruments when the markets become inactive and

quoted prices may reflect distressed transactions and (2) recording impairment charges on investments in debt

securities. The new guidance highlighted and expanded on the factors that should be considered in estimating fair

value when the volume and level of activity for a financial asset or liability has significantly decreased and

required new disclosures relating to fair value measurement inputs and valuation techniques (including changes

in inputs and valuation techniques). In addition, new guidance regarding recognition and presentation of other-

than-temporary impairments changed (1) the trigger for determining whether an other-than-temporary

impairment exists and (2) the amount of an impairment charge to be recorded in earnings. We adopted the

provisions of the new guidance for the quarter ended June 30, 2009. Refer to Note 4 and Note 5 to the

consolidated financial statements included in Item 8.—Financial Statements and Supplementary Data for

disclosures related to the implementation of the new guidance.

Under the revised other-than-temporary impairment model for debt securities held, we recognize an

impairment loss in income in an amount equal to the full difference between the amortized cost basis and the fair

value when we have the intent to sell the debt security or it is more likely than not we will be required to sell the

debt security before recovery of our amortized cost basis. However, if we do not intend to sell the debt security,

we evaluate the expected cash flows to be received as compared to amortized cost and determine if a credit loss

has occurred. In the event of a credit loss, only the amount of the impairment associated with the credit loss is

recognized currently in income with the remainder of the loss recognized in other comprehensive income.

When we do not intend to sell a security in an unrealized loss position, potential other-than-temporary

impairment is considered using a variety of factors, including the length of time and extent to which the fair

value has been less than cost; adverse conditions specifically related to the industry, geographic area or financial

condition of the issuer or underlying collateral of a security; payment structure of the security; changes in credit

rating of the security by the rating agencies; the volatility of the fair value changes; and changes in fair value of

72