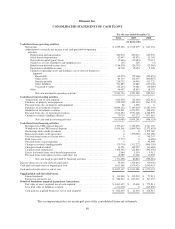

Humana 2010 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2010 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

Our strategy, long-range business plan, and annual planning process support our goodwill impairment tests.

These tests are performed, at a minimum, annually in the fourth quarter, and are based on an evaluation of future

discounted cash flows. We rely on this discounted cash flow analysis to determine fair value. However outcomes

from the discounted cash flow analysis are compared to other market approach valuation methodologies for

reasonableness. We use discount rates that correspond to a market-based weighted-average cost of capital and

terminal growth rates that correspond to long-term growth prospects, consistent with the long-term inflation rate.

Key assumptions in our cash flow projections, including changes in membership, premium yields, medical and

administrative cost trends, and certain government contract extensions, are consistent with those utilized in our

long-range business plan and annual planning process. If these assumptions differ from actual, including the

impact of the ultimate outcome of health care reform legislation the estimates underlying our goodwill

impairment tests could be adversely affected. Goodwill impairment tests completed in each of the last three years

did not result in an impairment loss. The fair value of our reporting units with significant goodwill exceeded

carrying amounts by a margin ranging from approximately 68% to 107%. A 100 basis point increase in the

discount rate would decrease this margin to a range of approximately 43% to 84%.

The ultimate loss of the TRICARE South Region contract would adversely affect $49.8 million of the

military services reporting unit’s goodwill. In July 2009, we were notified by the DoD that we were not awarded

the third generation TRICARE program contract for the South Region which had been subject to competing bids.

We filed a protest with the GAO in connection with the award to another contractor and in October 2009 we

learned that the GAO had upheld our protest, determining that the TMA evaluation of our proposal had

unreasonably failed to fully recognize and reasonably account for the likely cost savings associated with our

record of obtaining network provider discounts from our established network in the South Region. On

December 22, 2009, we were advised that TMA notified the GAO of its intent to implement corrective action

consistent with the discussion contained within the GAO’s decision with respect to our protest. On October 22,

2010, TMA issued its latest amendment to the request for proposal requesting from offerors final proposal

revisions to address, among other things, health care cost savings resulting from provider network discounts in

the South Region. We submitted our final proposal revisions on November 9, 2010. At this time, we are not able

to determine whether or not the protest decision by the GAO will have any effect upon the ultimate disposition of

the contract award.

On October 5, 2010, we were notified that the TMA intended to negotiate with us for an extension of our

administration of the TRICARE South Region contract scheduled to end on March 31, 2011, and on January 6,

2011, an Amendment of Solicitation/Modification of Contract to the TRICARE South Region contract, in the

form of an undefinitized contract action, became effective. The Amendment adds one additional one-year option

period, Option Period IX (which runs from April 1, 2011 through March 31, 2012). On January 21, 2011, the

TMA notified us of their intent to exercise Option Period IX. We will continue to assess the fair value of our

military services reporting unit each reporting period based on our estimate of future discounted cash flows

associated with the reporting unit, primarily derived from cash flows associated with the TRICARE South

Region contract. We will recognize a goodwill impairment if and when our impairment test indicates that the

carrying value of goodwill exceeds the implied fair value. If we are not ultimately awarded the new third

generation TRICARE program contract for the South Region, we expect that as the March 31, 2012 contract end

date nears, future cash flows will not be sufficient to warrant recoverability of all or a portion of the military

services goodwill. In this event, we expect a goodwill impairment would occur during the second half of 2011.

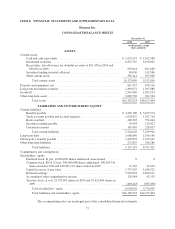

Refer to Note 16 to the consolidated financial statements included in Item 8.—Financial Statements and

Supplementary Data for further discussion of the TRICARE South Region contract.

Long-lived assets consist of property and equipment and other finite-lived intangible assets. These assets are

depreciated or amortized over their estimated useful life, and are subject to impairment reviews. We periodically

review long-lived assets whenever adverse events or changes in circumstances indicate the carrying value of the

asset may not be recoverable. In assessing recoverability, we must make assumptions regarding estimated future

cash flows and other factors to determine if an impairment loss may exist, and, if so, estimate fair value. We also

must estimate and make assumptions regarding the useful life we assign to our long-lived assets. If these

74