Humana 2010 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2010 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

markets. Further, various health insurance reform proposals are also emerging at the state level. It is reasonably

possible that the Health Insurance Reform Legislation and related regulations, as well as future legislative

changes, in the aggregate may have a material adverse effect on our results of operations, including restricting

revenue, enrollment and premium growth in certain products and market segments, restricting our ability to

expand into new markets, increasing our medical and administrative costs, lowering our Medicare payment rates

and increasing our expenses associated with the non-deductible federal premium tax and other assessments; our

financial position, including our ability to maintain the value of our goodwill; and our cash flows. If the new

non-deductible federal premium tax is imposed as enacted, and if we are unable to adjust our business model to

address this new tax, there can be no assurance that the non-deductible federal premium tax would not have a

material adverse effect on our results of operations, financial position, and cash flows.

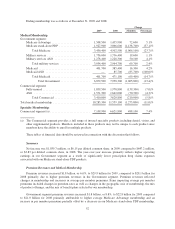

Government Segment

Our strategy and commitment to the Medicare programs have led to significant growth. Medicare

Advantage fully-insured membership increased to 1,733,800 members at December 31, 2010, up 225,300

members, or 14.9%, from 1,508,500 members at December 31, 2009, primarily due to sales of group Medicare

Advantage products and preferred provider organization, or PPO, products. Average fully-insured Medicare

Advantage membership increased 15.7% for the year ended December 31, 2010 compared to the year ended

December 31, 2009. Likewise, Medicare Advantage premium revenues have increased 17.5% to $19.3 billion for

the year ended December 31, 2010 from $16.4 billion for the year ended December 31, 2009. We expect

Medicare Advantage membership to increase by 90,000 to 110,000 members, or approximately 5% to 6% in

2011.

Beginning in 2011, sponsors of Medicare Advantage Private Fee-For-Service, or PFFS, plans are required to

contract with providers to establish adequate networks, except in geographic areas that CMS determines have

fewer than two network-based Medicare Advantage plans. Our development of networks in multiple areas of the

country over the past few years made it possible for many of our PFFS members to transition automatically to

our network-based products.

On April 5, 2010, CMS announced that Medicare Advantage payment rates would remain flat in 2011.

Based on the information available at the time we filed our 2011 bids in June 2010, we believe we effectively

designed Medicare Advantage products that address the flat rates while continuing to remain competitive

compared to both the combination of original Medicare with a supplement policy as well as other Medicare

Advantage competitors within our industry. In addition, we will continue to pursue our cost-reduction and

outcome-enhancing strategies, including care coordination and disease management, which we believe will

mitigate the adverse effects of the negative rate changes on our Medicare Advantage members. Nonetheless,

there can be no assurance that we will be able to successfully execute operational and strategic initiatives with

respect to changes in the Medicare Advantage program. Failure to execute these strategies may result in a

material adverse effect on our results of operations, financial position, and cash flows.

We also offer Medicare stand-alone prescription drug plans, or PDPs, under the Medicare Part D program.

These plans provide varying degrees of coverage. Our Medicare stand-alone PDP membership declined to

1,758,800 members at December 31, 2010, down 169,100 members, or 8.8%, from December 31, 2009, resulting

primarily from our competitive positioning as we realigned stand-alone PDP premium and benefit designs to

correspond with our historical prescription drug claims experience. In October 2010, we announced the lowest

premium national stand-alone Medicare Part D prescription drug plan co-branded with Wal-Mart Stores, Inc., the

Humana Walmart-Preferred Rx Plan, to be offered for the 2011 plan year. We expect Medicare stand-alone PDP

membership to increase between 525,000 and 575,000 members, or approximately 30% to 33% in 2011 primarily

due to increased sales, particularly for the Humana Walmart-Preferred Rx Plan.

Our quarterly Government segment earnings and operating cash flows are impacted by the Medicare Part D

benefit design and changes in the composition of our membership. The Medicare Part D benefit design results in

42