Humana 2010 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2010 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

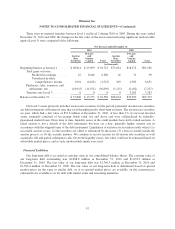

Humana Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Derivative Financial Instruments

At times, we may use interest-rate swap agreements to manage our exposure to interest rate risk. The

differential between fixed and variable rates to be paid or received is accrued and recognized over the life of the

agreements as adjustments to interest expense in the consolidated statements of income. Our interest-rate swap

agreements convert the fixed interest rates on our senior notes to a variable rate and are accounted for as fair

value hedges. Our interest-rate swap agreements, terminated in 2008, are more fully described in Note 12.

Stock-Based Compensation

We recognize stock-based compensation expense, as determined on the date of grant at fair value, straight-

line over the period during which an employee is required to provide service in exchange for the award (usually

the vesting period). We estimate expected forfeitures and recognize compensation expense only for those awards

which are expected to vest. We estimate the grant-date fair value of stock options using the Black-Scholes

option- pricing model. In addition, we report certain tax effects of stock-based compensation as a financing

activity rather than an operating activity in the consolidated statement of cash flows. Additional detail regarding

our stock-based compensation plans is included in Note 13.

Earnings Per Common Share

We compute basic earnings per common share on the basis of the weighted-average number of unrestricted

common shares outstanding. Diluted earnings per common share is computed on the basis of the weighted-

average number of unrestricted common shares outstanding plus the dilutive effect of outstanding employee

stock options and restricted shares using the treasury stock method.

Fair Value

Assets and liabilities measured at fair value are categorized into a fair value hierarchy based on whether the

inputs to valuation techniques are observable or unobservable. Observable inputs reflect market data obtained

from independent sources, while unobservable inputs reflect our own assumptions about the assumptions market

participants would use. The fair value hierarchy includes three levels of inputs that may be used to measure fair

value as described below.

Level 1 – Quoted prices in active markets for identical assets or liabilities. Level 1 assets and liabilities

include debt and equity securities that are traded in an active exchange market.

Level 2 – Observable inputs other than Level 1 prices such as quoted prices in active markets for similar

assets or liabilities, quoted prices for identical or similar assets or liabilities in markets that are not active, or

other inputs that are observable or can be corroborated by observable market data for substantially the full

term of the assets or liabilities. Level 2 assets and liabilities include debt securities with quoted prices that

are traded less frequently than exchange-traded instruments as well as debt securities and derivative

contracts whose value is determined using a pricing model with inputs that are observable in the market or

can be derived principally from or corroborated by observable market data.

Level 3 – Unobservable inputs that are supported by little or no market activity and are significant to the fair

value of the assets or liabilities. Level 3 includes assets and liabilities whose value is determined using

pricing models, discounted cash flow methodologies, or similar techniques reflecting our own assumptions

about the assumptions market participants would use as well as those requiring significant management

judgment.

89