Humana 2010 Annual Report Download - page 114

Download and view the complete annual report

Please find page 114 of the 2010 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

Humana Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

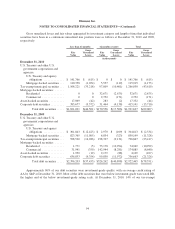

The terms of the new credit agreement include standard provisions related to conditions of borrowing,

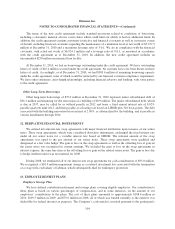

including a customary material adverse event clause which could limit our ability to borrow additional funds. In

addition, the credit agreement contains customary restrictive and financial covenants as well as customary events

of default, including financial covenants regarding the maintenance of a minimum level of net worth of $5,257.9

million at December 31, 2010 and a maximum leverage ratio of 3.0:1. We are in compliance with the financial

covenants, with actual net worth of $6,924.1 million and a leverage ratio of 0.8:1, as measured in accordance

with the credit agreement as of December 31, 2010. In addition, the new credit agreement includes an

uncommitted $250 million incremental loan facility.

At December 31, 2010, we had no borrowings outstanding under the credit agreement. We have outstanding

letters of credit of $10.4 million secured under the credit agreement. No amounts have ever been drawn on these

letters of credit. Accordingly, as of December 31, 2010, we had $989.6 million of remaining borrowing capacity

under the credit agreement, none of which would be restricted by our financial covenant compliance requirement.

We have other customary, arms-length relationships, including financial advisory and banking, with some parties

to the credit agreement.

Other Long-Term Borrowings

Other long-term borrowings of $37.0 million at December 31, 2010 represent junior subordinated debt of

$36.1 million and financing for the renovation of a building of $0.9 million. The junior subordinated debt, which

is due in 2037, may be called by us without penalty in 2012 and bears a fixed annual interest rate of 8.02%

payable quarterly until 2012, and then payable at a floating rate based on LIBOR plus 310 basis points. The debt

associated with the building renovation bears interest at 2.00%, is collateralized by the building, and is payable in

various installments through 2014.

12. DERIVATIVE FINANCIAL INSTRUMENTS

We entered into interest-rate swap agreements with major financial institutions upon issuance of our senior

notes. These swap agreements, which were considered derivative instruments, exchanged the fixed interest rate

under all our senior notes for a variable interest rate based on LIBOR. The notional amount of the swap

agreements was equal to the par amount of our senior notes. These swap agreements were qualified and

designated as a fair value hedge. The gain or loss on the swap agreements as well as the offsetting loss or gain on

the senior notes was recognized in current earnings. We included the gain or loss on the swap agreements in

interest expense, the same line item as the offsetting loss or gain on the related senior notes. The gain or loss due

to hedge ineffectiveness was not material for 2008.

During 2008, we terminated all of our interest-rate swap agreements for cash consideration of $93.0 million.

We recognized a $10.4 million impairment charge as a realized investment loss associated with the termination

of a swap with a subsidiary of Lehman, which subsequently filed for bankruptcy protection.

13. EMPLOYEE BENEFIT PLANS

Employee Savings Plan

We have defined contribution retirement and savings plans covering eligible employees. Our contribution to

these plans is based on various percentages of compensation, and in some instances, on the amount of our

employees’ contributions to the plans. The cost of these plans amounted to approximately $108.6 million in

2010, $109.5 million in 2009, and $79.6 million in 2008, all of which was funded currently to the extent it was

deductible for federal income tax purposes. The Company’s cash match is invested pursuant to the participant’s

104