Humana 2010 Annual Report Download - page 128

Download and view the complete annual report

Please find page 128 of the 2010 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

|

|

Humana Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

associated with our individual major medical policies were $179.8 million at December 31, 2010 and $128.3

million at December 31, 2009. In light of the Health Insurance Reform Legislation, including mandating that

80% of premium revenues be expended on medical costs for individual major medical policies beginning in

2011, we completed a deferred acquisition cost recoverability analysis for our individual major medical policies

during 2010. Our recoverability test indicated that a substantial portion of unamortized deferred acquisition costs

associated with the individual major medical block of business were not recoverable from future income. As a

result, during 2010 we recorded a write-down of deferred acquisition costs of $147.5 million with a

corresponding charge to selling, general and administrative expense.

19. REINSURANCE

Certain blocks of insurance assumed in acquisitions, primarily life, long-term care, and annuities in run-off

status, are subject to reinsurance where some or all of the underwriting risk related to these policies has been

ceded to a third party. In addition, a large portion of our reinsurance takes the form of 100% coinsurance

agreements where, in addition to all of the underwriting risk, all administrative responsibilities, including

premium collections and claim payment, have also been ceded to a third party. We acquired these policies and

related reinsurance agreements with the purchase of stock of companies in which the policies were originally

written. We acquired these companies for business reasons unrelated to these particular policies, including the

companies’ other products and licenses necessary to fulfill strategic plans.

A reinsurance agreement between two entities transfers the underwriting risk of policyholder liabilities to a

reinsurer while the primary insurer retains the contractual relationship with the ultimate insured. As such, these

reinsurance agreements do not completely relieve us of our potential liability to the ultimate insured. However,

given the transfer of underwriting risk, our potential liability is limited to the credit exposure which exists should

the reinsurer be unable to meet its obligations assumed under these reinsurance agreements.

Reinsurance recoverables represent the portion of future policy benefits payable that are covered by

reinsurance. Amounts recoverable from reinsurers are estimated in a manner consistent with the methods used to

determine future policy benefits payable as detailed in Note 2. Reinsurance recoverables, included in other long-

term assets, were $420.7 million at December 31, 2010 and $378.3 million at December 31, 2009. The

percentage of these reinsurance recoverables resulting from 100% coinsurance agreements was 52% at

December 31, 2010 and 59% at December 31, 2009. Premiums ceded were $33.7 million in 2010, $33.0 million

in 2009 and $34.2 million in 2008.

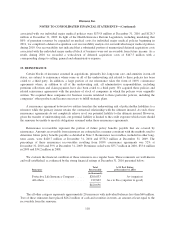

We evaluate the financial condition of these reinsurers on a regular basis. These reinsurers are well-known

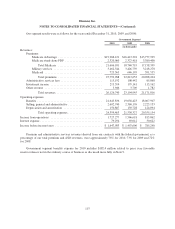

and well-established, as evidenced by the strong financial ratings at December 31, 2010 presented below:

Reinsurer

Total

Recoverable

A.M. Best Rating

at December 31, 2010

(in thousands)

Protective Life Insurance Company ...... $200,833 A+ (superior)

All others .......................... 219,863 A++ to B++ (superior to good)

$420,696

The all other category represents approximately 20 reinsurers with individual balances less than $60 million.

Two of these reinsurers have placed $26.2 million of cash and securities in trusts, an amount at least equal to the

recoverable from the reinsurer.

118