Electronic Arts 2015 Annual Report Download - page 106

Download and view the complete annual report

Please find page 106 of the 2015 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

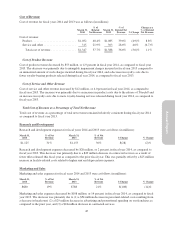

|

|

and the implementation of tax planning strategies. Evaluating and quantifying these amounts involves significant

judgments. Each source of income must be evaluated based on all positive and negative evidence; this evaluation

involves assumptions about future activity. Certain taxable temporary differences that are not expected to reverse

during the carry forward periods permitted by tax law cannot be considered as a source of future taxable income

that may be available to realize the benefit of deferred tax assets.

In fiscal year 2015, we reported U.S. pre-tax income, compared to pre-tax losses in each of the last seven fiscal

years. We have not yet been able to establish a sustained level of profitability in the U.S. or other sufficient

significant positive evidence to conclude that our U.S. deferred tax assets are more likely than not to be realized.

Therefore, we continue to maintain a valuation allowance against most of our U.S. deferred tax assets. It is

reasonably possible that in fiscal year 2016 we will establish a sustained level of profitability in the U.S. As a

result, it is possible that a significant portion of the $539 million valuation allowance recorded against our U.S.

deferred tax assets at March 31, 2015 could be reversed by the end of fiscal year 2016.

In the ordinary course of our business, there are many transactions and calculations where the tax law and

ultimate tax determination is uncertain. As part of the process of preparing our Consolidated Financial

Statements, we are required to estimate our income taxes in each of the jurisdictions in which we operate prior to

the completion and filing of tax returns for such periods. This process requires estimating both our geographic

mix of income and our uncertain tax positions in each jurisdiction where we operate. These estimates involve

complex issues and require us to make judgments about the likely application of the tax law to our situation, as

well as with respect to other matters, such as anticipating the positions that we will take on tax returns prior to

our actually preparing the returns and the outcomes of disputes with tax authorities. The ultimate resolution of

these issues may take extended periods of time due to examinations by tax authorities and statutes of limitations.

In addition, changes in our business, including acquisitions, changes in our international corporate structure,

changes in the geographic location of business functions or assets, changes in the geographic mix and amount of

income, as well as changes in our agreements with tax authorities, valuation allowances, applicable accounting

rules, applicable tax laws and regulations, rulings and interpretations thereof, developments in tax audit and other

matters, and variations in the estimated and actual level of annual pre-tax income can affect the overall effective

income tax rate.

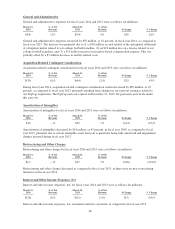

Impact of Recently Issued Accounting Standards

In April 2015, the FASB issued ASU 2015-03, Interest — Imputation of Interest (Topic 835-30), which requires

that debt issuance costs related to a recognized debt liability be presented in the balance sheet as a direct

deduction from the carrying amount of that debt liability, consistent with debt discounts. The recognition and

measurement guidance for debt issuance costs are not affected by this ASU. The disclosure requirements will be

effective for annual periods (and interim periods within those annual periods) beginning after December 15,

2015, and will require retrospective application. Early adoption is permitted. We do not expect the adoption to

have a material impact on our Consolidated Financial Statements.

In May 2014, the FASB issued ASU No. 2014-09, Revenue from Contracts with Customers (Topic 606), which

requires an entity to recognize the amount of revenue to which it expects to be entitled for the transfer of

promised goods or services to customers. The ASU will replace most existing revenue recognition guidance in

U.S. GAAP when it becomes effective. The standard permits the use of either the retrospective or cumulative

effect transition method. The Company is evaluating the effect that ASU 2014-09 will have on its Consolidated

Financial Statements and related disclosures. The Company has not yet selected a transition method nor has it

determined the effect of the standard on its ongoing financial reporting. The new standard is effective for annual

reporting periods beginning after December 15, 2016. Early application is not permitted. We are required to

adopt this standard in the first quarter of fiscal year 2018; however, in April 2015, the FASB issued an exposure

draft that would provide us with the option to adopt in either the first quarter of fiscal year 2018 or fiscal year

2019. We have not determined which of these two fiscal years we would adopt if the exposure draft is issued as

final in its current form.

36