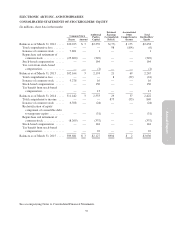

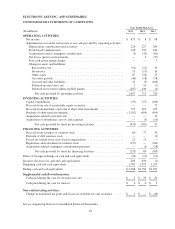

Electronic Arts 2015 Annual Report Download - page 137

Download and view the complete annual report

Please find page 137 of the 2015 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

Annual Report

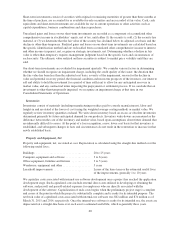

U.S. GAAP when it becomes effective. The standard permits the use of either the retrospective or cumulative

effect transition method. The Company is evaluating the effect that ASU 2014-09 will have on its Consolidated

Financial Statements and related disclosures. The Company has not yet selected a transition method nor has it

determined the effect of the standard on its ongoing financial reporting. The new standard is effective for annual

reporting periods beginning after December 15, 2016. Early application is not permitted. We are required to

adopt this standard in the first quarter of fiscal year 2018; however, in April 2015, the FASB issued an exposure

draft that would provide us with the option to adopt in either the first quarter of fiscal year 2018 or fiscal year

2019. We have not determined which of these two fiscal years we would adopt if the exposure draft is issued as

final in its current form.

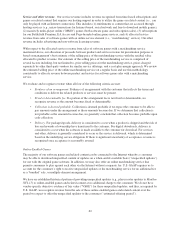

(2) FAIR VALUE MEASUREMENTS

There are various valuation techniques used to estimate fair value, the primary one being the price that would be

received from selling an asset or paid to transfer a liability in an orderly transaction between market participants

at the measurement date. When determining fair value, we consider the principal or most advantageous market in

which we would transact and consider assumptions that market participants would use when pricing the asset or

liability. We measure certain financial and nonfinancial assets and liabilities at fair value on a recurring and

nonrecurring basis.

Fair Value Hierarchy

The three levels of inputs that may be used to measure fair value are as follows:

•Level 1. Quoted prices in active markets for identical assets or liabilities.

•Level 2. Observable inputs other than quoted prices included within Level 1, such as quoted prices for

similar assets or liabilities, quoted prices in markets with insufficient volume or infrequent transactions

(less active markets), or model-derived valuations in which all significant inputs are observable or can be

derived principally from or corroborated with observable market data for substantially the full term of the

assets or liabilities.

•Level 3. Unobservable inputs to the valuation methodology that are significant to the measurement of the

fair value of assets or liabilities.

67