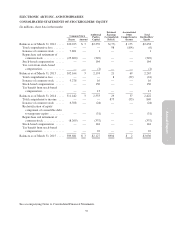

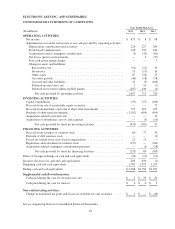

Electronic Arts 2015 Annual Report Download - page 136

Download and view the complete annual report

Please find page 136 of the 2015 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

|

|

Income Taxes

We recognize deferred tax assets and liabilities for both the expected impact of differences between the financial

statement amount and the tax basis of assets and liabilities and for the expected future tax benefit to be derived

from tax losses and tax credit carryforwards. We record a valuation allowance against deferred tax assets when it

is considered more likely than not that all or a portion of our deferred tax assets will not be realized. In making

this determination, we are required to give significant weight to evidence that can be objectively verified. It is

generally difficult to conclude that a valuation allowance is not needed when there is significant negative

evidence, such as cumulative losses in recent years. Forecasts of future taxable income are considered to be less

objective than past results, therefore, cumulative losses weigh heavily in the overall assessment.

In addition to considering forecasts of future taxable income, we are also required to evaluate and quantify other

possible sources of taxable income in order to assess the realization of our deferred tax assets, namely the

reversal of existing deferred tax liabilities, the carry back of losses and credits as allowed under current tax law,

and the implementation of tax planning strategies. Evaluating and quantifying these amounts involves significant

judgments. Each source of income must be evaluated based on all positive and negative evidence; this evaluation

involves assumptions about future activity. Certain taxable temporary differences that are not expected to reverse

during the carry forward periods permitted by tax law cannot be considered as a source of future taxable income

that may be available to realize the benefit of deferred tax assets.

In fiscal year 2015, we reported U.S. pre-tax income, compared to pre-tax losses in each of the last seven fiscal

years. We have not yet been able to establish a sustained level of profitability in the U.S. or other sufficient

significant positive evidence to conclude that our U.S. deferred tax assets are more likely than not to be realized.

Therefore, we continue to maintain a valuation allowance against most of our U.S. deferred tax assets. However,

it is reasonably possible that in fiscal year 2016 we will establish a sustained level of profitability in the U.S. As

a result, it is possible that a significant portion of the valuation allowance recorded against our U.S. deferred tax

assets at March 31, 2015 could be reversed by the end of fiscal year 2016.

Recently Adopted Accounting Standards

On April 1, 2014, we adopted ASU 2013-11, Presentation of an Unrecognized Tax Benefit When a Net

Operating Loss Carryforward, a Similar Tax Loss, or a Tax Credit Carryforward Exists. Under the new

accounting standard, an unrecognized tax benefit is required to be presented as a reduction to a deferred tax asset

if the disallowance of the uncertain tax position would reduce an available tax loss or tax credit carryforward

instead of resulting in a cash tax liability. The ASU applies prospectively to all unrecognized tax benefits that

exist as of the adoption date. As a result of the adoption, we reduced: (a) noncurrent income tax obligations by

$96 million; (b) current deferred income tax assets by $18 million; and (c) noncurrent deferred income tax assets

by $11 million. We increased noncurrent deferred income tax liabilities by $67 million. As the new accounting

standard only impacted presentation, it did not have an impact on the Company’s net financial position, results of

operations, or cash flows.

Impact of Recently Issued Accounting Standards

In April 2015, the FASB issued ASU 2015-03, Interest — Imputation of Interest (Topic 835-30), which requires

that debt issuance costs related to a recognized debt liability be presented in the balance sheet as a direct

deduction from the carrying amount of that debt liability, consistent with debt discounts. The recognition and

measurement guidance for debt issuance costs are not affected by this ASU. The disclosure requirements will be

effective for annual periods (and interim periods within those annual periods) beginning after December 15,

2015, and will require retrospective application. Early adoption is permitted. We do not expect the adoption to

have a material impact on our Consolidated Financial Statements.

In May 2014, the FASB issued ASU No. 2014-09, Revenue from Contracts with Customers (Topic 606), which

requires an entity to recognize the amount of revenue to which it expects to be entitled for the transfer of

promised goods or services to customers. The ASU will replace most existing revenue recognition guidance in

66