Philips 2007 Annual Report Download - page 136

Download and view the complete annual report

Please find page 136 of the 2007 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

|

|

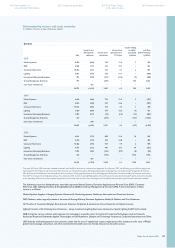

Philips Annual Report 2007142

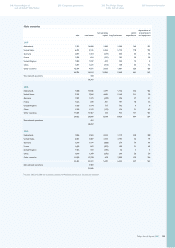

2005

Net income

As reported 2,868

Add: Stock-based compensation expenses included in

reported net income, net of related taxes 65

Deduct: stock-based compensation expenses

determined using the fair-value method,

net of related taxes (77)

Pro forma 2,856

Basic earnings per share (in euros):

As reported 2.29

Pro forma 2.28

Diluted earnings per share (in euros):

As reported 2.29

Pro forma 2.28

The fair value of the amount payable to employees in respect of share-

based payments which are settled in cash is recognized as an expense,

with a corresponding increase in liabilities, over the vesting period.

The liability is remeasured at each reporting date and at settlement

date. Any changes in fair value of the liability are recognized as

compensation expense in the income statement.

Research and development

Costs of research and development are expensed in the period

in which they are incurred.

Advertising

Advertising costs are expensed as incurred.

Leases

Leases in which a signicant portion of the risks and rewards of

ownership are retained by the lessor are classied as operating leases.

Payments made under operating leases are recognized in the income

statement on a straight-line basis over the term of the lease.

Leases in which the Company has substantially all the risk and rewards

of ownership are classied as nance leases. Finance leases are

capitalized at the lease’s commencement at the lower of the fair value

of leased property and the present value of the minimum lease payments.

Each lease payment is allocated between the liability and nance charges

so as to achieve a constant rate of interest on the nance balance

liabilities. The property, plant and equipment acquired under nance

leases is depreciated over the shorter of the useful life of the assets

and the lease term.

Income taxes

Income taxes are accounted for using the asset and liability method.

Income tax is recognized in the income statement except to the

extent that it relates to an item recognized directly within stockholders’

equity, including other comprehensive income (loss), in which case

the related tax effect is also recognized there. Current-year deferred

taxes related to prior-year equity items which arise from changes in tax

rates or tax laws are included in income. Current tax is the expected

tax payable on the taxable income for the year, using tax rates enacted

at the balance sheet date, and any adjustment to tax payable in respect

of previous years. Deferred tax assets and liabilities are recognized

for the expected tax consequences of temporary differences between

the tax bases of assets and liabilities and their reported amounts.

Measurement of deferred tax assets and liabilities is based on the

enacted tax rates expected to apply to taxable income in the years

in which those temporary differences are expected to be recovered

or settled. Deferred tax assets, including assets arising from loss carry-

forwards, are recognized, net of a valuation allowance, if it is more

likely than not that the asset or a portion thereof will not be realized.

Deferred tax assets and liabilities are not discounted.

Deferred tax liabilities for withholding taxes are recognized for

subsidiaries in situations where the income is to be paid out as

dividends in the foreseeable future, and for undistributed earnings

of unconsolidated companies.

Changes in tax rates are reected in the period in which such change

is enacted.

Uncertain tax position

Income tax benet from an uncertain tax position is recognized only

if it is more likely than not that the tax position will be sustained upon

examination by the relevant taxing authorities, based on the technical

merits of the position. The income tax benet recognized in the nancial

statements from such position is measured based on the largest benet

that is more than 50% likely to be realized upon settlement with a taxing

authority that has full knowledge of all relevant information. The

liability for unrecognized tax benets, including related interest and

penalties, is recorded as other non-current liabilities. Interest is

presented as part of nancial expenses while penalty is classied

as part of current tax expense in the income statement.

Derivative nancial instruments

The Company uses derivative nancial instruments principally for the

management of its foreign currency risks and to a more limited extent

for interest rate and commodity price risks. All derivative nancial

instruments are classied as assets or liabilities and are accounted

for at trade date. The Company measures all derivative nancial

instruments based on fair values derived from market prices of the

instruments or from option pricing models, as appropriate. Changes

in the fair value of a derivative that is highly effective and that is

designated and qualies as a fair value hedge, along with the loss or

gain on the hedged asset, liability or unrecognized rm commitment of

the hedged item that is attributable to the hedged risk, are recorded in

the income statement. Gains or losses arising from changes in fair

value of derivatives are recognized in the income statement, except

for derivatives that are highly effective and qualify for cash ow or

net investment hedge accounting.

Changes in the fair value of a derivative that is highly effective and

that is designated and qualies as a cash ow hedge, are recorded in

accumulated other comprehensive income, until earnings are affected

by the variability in cash ows of the designated hedged item.

Changes in the fair value of derivatives that are highly effective as

hedges and that are designated and qualify as foreign currency hedges

are recorded in either earnings or accumulated other comprehensive

income, depending on whether the hedge transaction is a fair value

hedge or a cash ow hedge.

The Company formally assesses, both at the hedge’s inception and

on an ongoing basis, whether the derivatives that are used in hedging

transactions are highly effective in offsetting changes in fair values or

cash ows of hedged items. When it is established that a derivative

is not highly effective as a hedge or that it has ceased to be a highly

effective hedge, the Company discontinues hedge accounting

prospectively. When hedge accounting is discontinued because it has

been established that the derivative no longer qualies as an effective

fair value hedge, the Company continues to carry the derivative on

the balance sheet at its fair value, and no longer adjusts the hedged

asset or liability for changes in fair value. When hedge accounting is

discontinued because it is probable that a forecasted transaction will

not occur within a period of two months from the originally forecasted

transaction date, the Company continues to carry the derivative

on the balance sheet at its fair value, and gains and losses that

were accumulated in other comprehensive income are recognized

immediately in the income statement. In all other situations in which

hedge accounting is discontinued, the Company continues to carry

the derivative at its fair value on the balance sheet, and recognizes

any changes in its fair value in the income statement.

Foreign currency differences arising on the translation of a nancial

liability designated as a hedge of a net investment in a foreign

operation are recognized directly as a separate component of equity,

to the extent that the hedge is effective. To the extent that the hedge

is ineffective, such differences are recognized in the income statement.

For interest rate swaps designated as a fair value hedge of an

interest-bearing asset or liability that are unwound, the amount of

the fair value adjustment to the asset or liability for the risk being

hedged is released to the income statement over the remaining life

of the asset or liability based on the recalculated effective yield.

Non-derivative nancial instruments

Non-derivative nancial instruments are recognized initially at

cost or fair value. Financial assets transferred to another party are

derecognized to the extent that the Company surrenders control

over those assets in exchange for a consideration other than benecial

exchange for interest in the transferred assets. Financial liabilities are

128 Group nancial statements

Signicant accounting policies

188 IFRS information 240 Company nancial statements