Philips 2007 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2007 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

|

|

Philips Annual Report 200742

Net income

In 2007, income from continuing operations amounted

to EUR 4,601 million, an increase of EUR 3,700 million

compared with 2006. The improvement was driven by

EUR 651 million higher EBIT and a EUR 2,585 million

increase in nancial income, primarily due to the sale

of shares in TSMC. The EUR 455 million higher income

tax charges were more than offset by a EUR 920 million

increase in results relating to equity-accounted investees,

which included a EUR 508 million gain on the sale of

shares of LG.Philips LCD as well as a EUR 456 million

increase in that company’s operational results.

The loss from discontinued operations amounted

to EUR 433 million, mainly due to the aforementioned

MedQuist-related losses, whereas 2006 included a total

gain of EUR 4,283 million from the sale of a majority

stake in the Semiconductors division.

Net income for the Group showed a prot of

EUR 4,168 million, or EUR 3.84 per common share,

compared to EUR 5,383 million, or EUR 4.58 per

common share, in 2006.

Performance by market cluster

Philips monitors its performance on a geographical axis

based on the following market clusters:

key emerging markets, including China, India and Latin•

America

other emerging markets, including emerging markets •

in Central and Eastern Europe, Russia, Ukraine and

Central Asia, the Middle East and Africa, Turkey and

the ASEAN zone

mature markets, including Western Europe, North •

America, Japan, Korea, Australia and New Zealand.

In 2007, sales growth was particularly strong in emerging

markets, which will continue to be a focal area of growth

for Philips. Emerging markets, most notably China, Russia

and India, contributed 60% to our comparable sales

increase in value, while accounting for approximately

one third of total revenues.

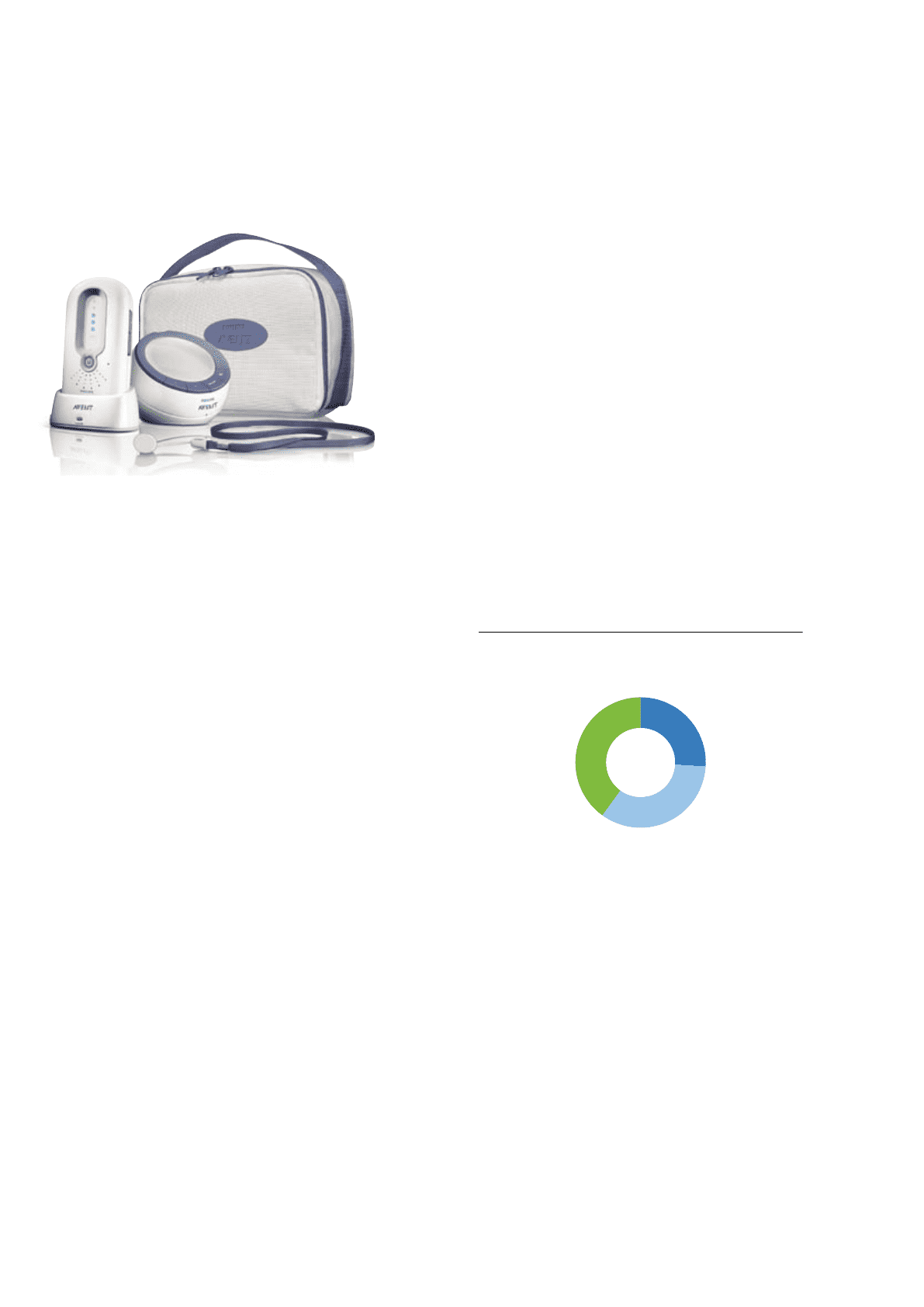

Comparable sales value growth 2007

per market cluster, in % of total

key emerging markets

26%

other emerging markets

34%

mature markets

40%

Key emerging markets showed strong comparable

growth, primarily driven by Lighting, Medical Systems

and DAP, partly offset by a sales decline at CE, mainly

due to Connected Displays in Latin America.

Other emerging markets delivered strong double-digit

sales growth compared to 2006, driven by the outstanding

performance of DAP and CE as well as robust expansion

of Lighting and Medical Systems in these countries.

Sales in Western Europe showed a solid increase on

a comparable basis, visible in all sectors, most notably

the double-digit increase at DAP, followed by good

performances by CE, Lighting and Medical Systems.

The market launch of the rst dual-branded products

in September made the combined strengths of Philips and

Avent clearly visible to our consumers.

8 Financial highlights 10 Message from the President 16 The Philips Group

Management discussion

and analysis

62 The Philips sectors