Philips 2007 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2007 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

|

|

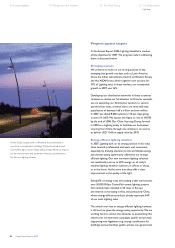

Philips Annual Report 2007 87Philips Annual Report 2007 87

Sales and net operating capital

in billions of euros

Sales NOC

7

6

5

4

3

2

1

0

4.5

1.5

2003

4.5

1.5

2004

4.8

2.5

2005

5.5

2.5

2006

6.1

3.9

2007

EBIT and EBITA

in millions of euros

EBITA in valueEBIT in value EBITA as a % of sales

0

200

400

600

800

2003

528

528

11.7

12.0

10.6

11.1

11.9

2004

542

541

2005

508

499

2006

608

577

2007

722

675

growth across all businesses except for Special Lighting

Applications in Asia, related to the rapid contraction

of the rear-projection TV market. Sales growth was

notably strong in China (18%) and India (16%).

EBITA in 2007 amounted to EUR 722 million, growing

by EUR 114 million year-on-year to reach 11.9% of sales,

compared to EUR 608 million or 11.1% in 2006. This

improvement was driven by solid earnings growth at

Lamps and Luminaires, additional EBITA following the

successful integration of PLI, and lower losses related

to the uorescent-based backlighting solutions business

which we exited in Q1 2007.

EBIT improved by EUR 98 million to reach EUR 675

million, or 11.1% of sales. Restructuring charges, purchase-

accounting-related charges and other net incidental items

totaled EUR 55 million, compared to EUR 48 million in 2006.

Cash ows before nancing included acquisition-related

investments totaling EUR 1,162 million in 2007, most

notably the net payments of EUR 561 million for Partners

in Lighting International and of EUR 515 million for

Color Kinetics. Net capital expenditures declined by

EUR 88 million compared to 2006, mainly due to higher

investments in Lumileds in 2006.

Net inventories increased to 15.4% of sales, compared

to 13.5% in 2006, primarily due to higher inventory levels

within PLI (due to rapid order ful llment requirements

and above-average lead times from PLI-owned factories

in China) and at Lamps (due to increased lead times

resulting from the transfer of the production of energy-

ef cient lamps to Asia).

Strategy and 2008 objectives

Philips Lighting will play an important role in the realization

of Philips’ Vision 2010 ambition. For 2008 and beyond,

Lighting has put in place a number of speci c value-creating

initiatives which it will drive through a framework of

Growth, Talent and Simplicity:

Accelerate growth, both organically and through •

the successful integration of acquisitions, on the basis

of strength in emerging markets and in energy-ef cient

lighting solutions

Expand in the direction of system solutions, closely •

connected to the applications in the market, in the areas

of professional luminaires and consumer luminaires

Continue to build on the leading position in •

solid-state lighting

Strengthen the leadership bench via proactive •

talent recruitment

Continue to build on the strong culture of excellence, •

while creating a learning organization focused on

continuous improvement

Streamline ways of working by implementing segment •

marketing, strengthening customer focus and driving

for supply excellence.

98 Risk management 112 Our leadership 116 Report of the Supervisory Board 126 Financial Statements