Philips 2007 Annual Report Download - page 69

Download and view the complete annual report

Please find page 69 of the 2007 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

|

|

Philips Annual Report 2007 75Philips Annual Report 2007 75

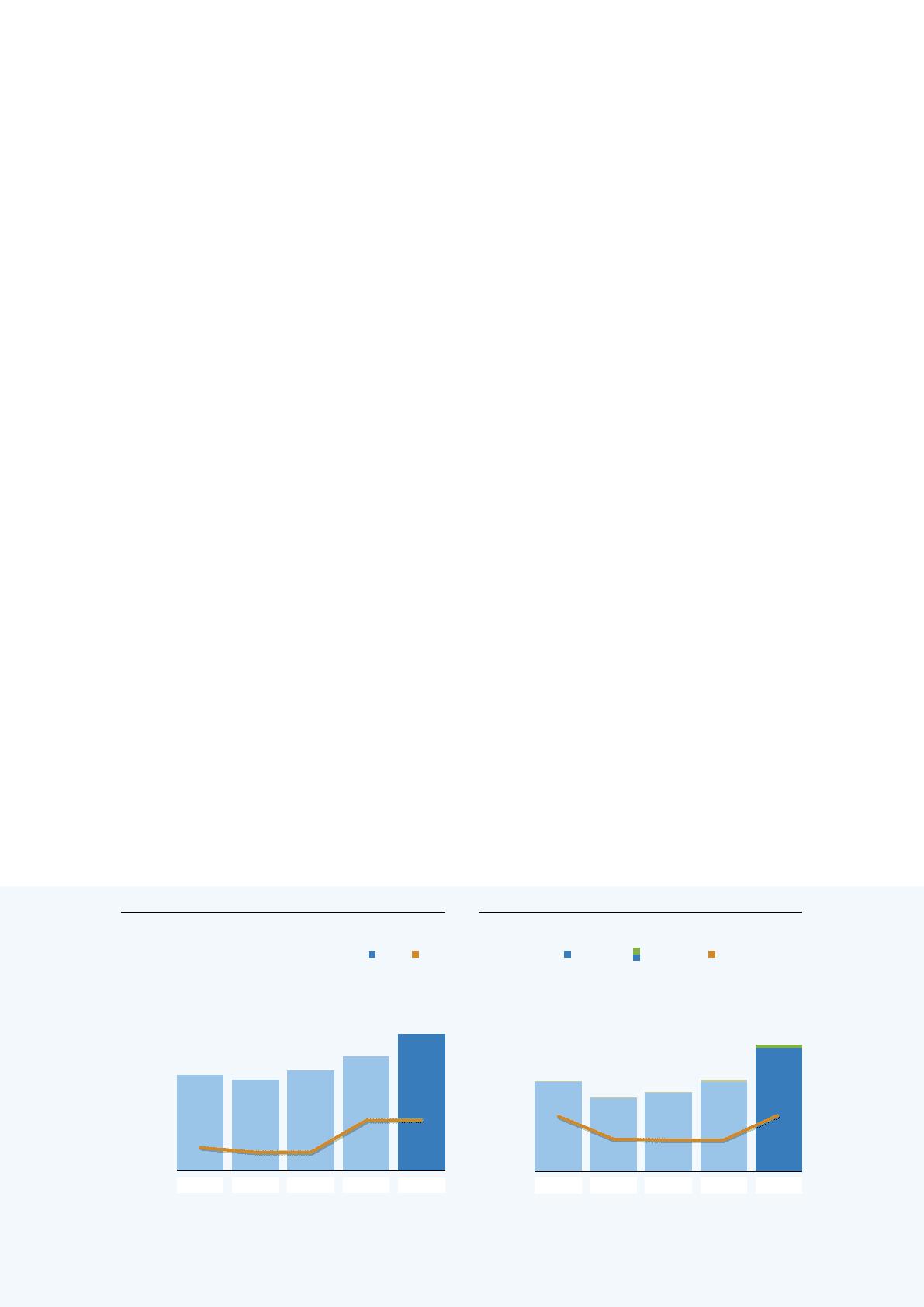

Sales and net operating capital

in billions of euros

Sales NOC

4

3

2

1

0

2.1

0.5

2003

2.0

0.4

2004

2.2

0.4

2005

2.5

1.1

2006

3.0

1.1

2007

EBIT and EBITA

in millions of euros

EBITA in valueEBIT in value EBITA as a % of sales

0

150

300

450

600

2003

2004

2005

328

324

2006

378

370

2007

523

510

373

368

306

15.0

14.9

17.6

17.5

15.0

301

Compared to 2006, EBITA increased by EUR 145 million

to EUR 523 million, corresponding to a pro tability

improvement of 2.7% of sales, reaching 17.6% of sales

in 2007, well above the targeted 15%. The year-on-year

earnings rise was largely driven by higher sales and tight

cost management. EBITA improvements were visible – both

in absolute amounts and relative to sales – in all businesses.

EBIT increased by EUR 140 million to EUR 510 million

in 2007, compared to EUR 370 million in 2006.

DAP generated EUR 415 million cash ows before

nancing activities, broadly in line with last year,

excluding the EUR 689 million net cash payment

for the acquisition of Avent. Higher earnings were

largely offset by increased working capital needs.

Strategy and 2008 objectives

Following the announcement of Vision 2010 in September

2007, the former Consumer Electronics and Domestic

Appliances and Personal Care divisions have been

integrated effective January 1, 2008, and going

forward

will be reported as the Consumer Lifestyle sector.

Philips Consumer Lifestyle will play an important role

in the realization of Philips’ Vision 2010 ambition.

For 2008 and beyond, Consumer Lifestyle has put

in place a number of speci c value-creating initiatives

which it will drive through a framework of Growth,

Talent and Simplicity:

Leverage post-integration synergies, particularly •

with regard to customers, markets and key account

management, as well as in supply chain optimization

and the sector’s relationships with third-party suppliers

and partners; synergies will also be realized across

all operational processes, through the organizational

blueprint and way-of-working design

Open up new value spaces in the consumer lifestyle •

eld to further strengthen our business portfolio

and to deliver upon our growth ambition

Create a uni ed, engaged and high-performance •

organization in which growth and diversity can

be nurtured within our leadership community

and talent pipeline

Maximize our structure to be fully market-driven, •

in terms of our customer relationships and our

business portfolio.

98 Risk management 112 Our leadership 116 Report of the Supervisory Board 126 Financial Statements