Philips 2007 Annual Report Download - page 9

Download and view the complete annual report

Please find page 9 of the 2007 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

|

|

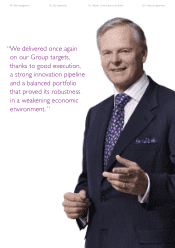

companies. Our ambition and your expectation are clearly

higher, and so with our agenda for 2008 we will drive even

more relentlessly for value creation and delivery.

Performance against targets

As I do every year, I would also like to update you on

how we did on the things we had set out to do as part

of our 2007 Management Agenda.

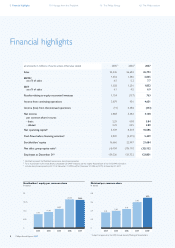

Maintain annual average sales growth of 5-6% and achieve

above 7.5% EBITA

I am glad to say we achieved our Group targets of 5-6%

annual average sales growth and EBITA above 7.5%.

At 5%, comparable sales growth was at the low end

of the bandwidth as particularly high growth at DAP and

solid growth at Lighting were offset by a at performance

at Consumer Electronics, caused by a loss of market

share in the rst half of the year at Connected Displays

– a highly competitive business that we continue to

manage for protability – while Medical Systems’ sales

growth was hampered by a declining US imaging market,

triggered by the Decit Reduction Act.

At 7.7% of sales, our EBITA margin is the highest in

recent years, up from 5.2% in 2006 – an excellent

starting position towards our 2010 targets. Operationally,

we executed very well in our DAP and Lighting businesses,

which achieved EBITA margins of 17.6% and 11.9%

respectively, even though Lighting was hampered by the

sharp decline in the very protable UHP business and

the closure of our LCD backlighting activity. However,

we had some issues at Consumer Electronics, especially

Connected Displays, with losses in the US for the whole

year. Despite this, Consumer Electronics managed to

exceed its target of 3% EBITA margin. At Medical Systems

we were impacted by the slowdown of the US imaging

market. The shortfall in the US could not be compensated

entirely by a good operational performance of the non-

imaging businesses and in the rest of the world, which

resulted in slight under-performance against margin

targets, EBITA remaining virtually stable at 13.5%.

Delivering on our 2007 objectives puts us in a good

starting position to meet the more ambitious medium-

term targets set as part of Vision 2010, especially as this

portfolio of activities has shown resilience in earlier

periods of economic downturn.

Continue to redeploy capital in a disciplined way through

value-creating acquisitions, share buy-backs and dividends

In 2007 we continued to further strengthen our key

businesses and create true market leadership positions

by means of both small ‘ll-in’ and larger ‘platform’

acquisitions – all high-growth high-margin businesses.

Besides our acquisition drive, which resulted in 2007

in a total cash-out of EUR 1.5 billion, we continued our

policy of repurchasing shares, buying back some EUR 1.6

billion worth of shares, of which EUR 0.8 million for

cancellation. Unfortunately the buy-back through the

so-called ‘second trading line’ brought us only about

half of the EUR 1.6 billion we had targeted. However,

on the back of a change to Dutch tax law, we were able,

in December, to announce a new EUR 5 billion buy-back

plan, through which we will more than catch up on

our target.

With our year-end announcements of the Respironics

acquisition and our latest share buy-back plan, we passed

the EUR 10 billion mark twice – for closed and announced

acquisitions, as well as for the total of realized and intended

share buy-backs. In total we have re-allocated over

EUR 20 billion of capital since 2005, largely completing

our capital re-allocation program and putting us well

on track to deliver, as promised, an efcient balance

sheet before the end of 2009.

With our strong focus on economic value added as well

as return on invested capital, our projections show that

Philips Annual Report 200712

8 Financial highlights 10 Message from the President 16 The Philips Group 62 The Philips sectors