Philips 2007 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2007 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

|

|

Philips Annual Report 2007 69

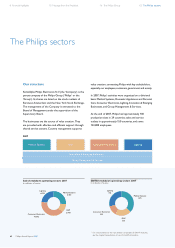

Sales and net operating capital

in billions of euros

Sales NOC

8

6

4

2

0

5.6

2.8

20031)

5.5

2.6

20041)

6.0

3.2

20051)

6.4

4.1

20061)

6.5

4.1

2007

0

250

500

750

1,000

EBIT and EBITA

in millions of euros

EBITA in valueEBIT in value EBITA as a % of sales

2007

875

743

454

2003

1)

768

688

2005

1)

861

734

2006

1)

2004

1)

539

538

616

9.7

11.2

12.8

13.4

13.5

1) Restated to present the MedQuist business as a discontinued operation 1) Restated to present the MedQuist business as a discontinued operation

Philips Annual Report 2007 69

For 2008, strong sales growth is anticipated in Patient

Monitoring, Cardiac Care, Home Healthcare Solutions

and Customer Services, tempered by limited growth in

Imaging Systems.

Regulatory requirements

Medical Systems is subject to extensive regulation.

It strives for full compliance with regulatory product

approval and quality system requirements in every

market it serves by addressing speci c terms and

conditions of local ministry of health or federal

regulatory authorities, including agencies like the US

FDA, EU Competent Authorities and Japanese MLHW.

Environmental and sustainability requirements like the

European Union’s Waste from Electrical and Electronic

Equipment (WEEE) and the Restriction of Hazardous

Substances (RoHS) directives are met with comprehensive

EcoDesign and manufacturing programs to reduce the

use of hazardous materials.

Continuous clinical innovation and breakthroughs,

in combination with collaborative customer relationships,

drive growth and pro tability. However, the success of

clinical innovation is often dependent upon appropriate

reimbursement. In the US, concern over rapid and

sustained growth in imaging services has attracted

increased scrutiny by the Federal government and

commercial payers. This has resulted in the adoption

of new strategies designed to curb growth that could

continue to impact Philips Healthcare in 2008 and

beyond. The De cit Reduction Act of 2005 came into

effect in February 2006 and included substantial reductions

in Medicare payments for imaging services performed

in non-hospital settings. Commercial payers are also

implementing several types of utilization management

strategies designed to curb growth. Philips will continue to

work closely with legislators, payers and providers to avoid

further unwarranted reimbursement reductions and to

ensure a more rational approach to payment for innovative

technologies, particularly advanced imaging services.

Strategy and 2008 objectives

Following the announcement of Vision 2010 in

September 2007, the former Medical Systems division

and Consumer Healthcare Solutions business – now

renamed Home Healthcare Solutions – have been

integrated effective January 1, 2008, and going forward

will be reported as the Healthcare sector.

Philips Healthcare will play an important role in the

realization of Philips’ Vision 2010 ambition. For 2008

and beyond, Healthcare has put in place a number

of speci c value-creating initiatives which it will drive

through a framework of Growth, Talent and Simplicity:

Extract value from acquisitions through successful •

integration

Expand presence in emerging markets•

Cultivate leadership talent and recognize and reward •

top talent

Deliver on care cycle solutions from the hospital •

to the home.

98 Risk management 112 Our leadership 116 Report of the Supervisory Board 126 Financial Statements