Humana 2013 Annual Report Download - page 141

Download and view the complete annual report

Please find page 141 of the 2013 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

|

|

Humana Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

In addition, we establish reserves for future policy benefits in recognition of the fact that some of the

premium received in the earlier years is intended to pay anticipated benefits to be incurred in future years. At

policy issuance, these reserves are recognized on a net level premium method based on interest rates, mortality,

morbidity, and maintenance expense assumptions. The assumptions used to determine the liability for future

policy benefits are established and locked in at the time each contract is issued and only change if our expected

future experience deteriorates to the point that the level of the liability, together with the present value of future

gross premiums, are not adequate to provide for future expected policy benefits and maintenance costs (i.e. the

loss recognition date).

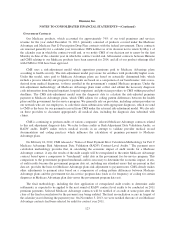

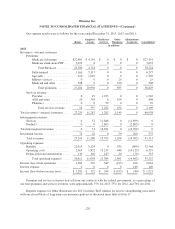

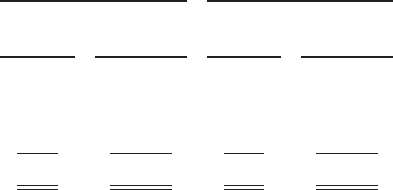

The table below presents deferred acquisition costs and future policy benefits payable associated with our

long-duration insurance products for the years ended December 31, 2013 and 2012.

2013 2012

Deferred

acquisition

costs

Future policy

benefits

payable

Deferred

acquisition

costs

Future policy

benefits

payable

(in millions)

Other long-term assets ............................. $166 $ 0 $149 $ 0

Trade accounts payable and accrued expenses ........... 0 (67) 0 (63)

Long-term liabilities ............................... 0 (2,207) 0 (1,858)

Total asset (liability) ........................... $166 $(2,274) $149 $(1,921)

In addition, future policy benefits payable include amounts of $215 million at December 31, 2013 and $220

million at December 31, 2012 which are subject to 100% coinsurance agreements as more fully described in Note 18.

Benefits expense associated with future policy benefits payable was $354 million in 2013, $136 million in

2012, and $114 million in 2011. Benefits expense for 2013 included net charges of $243 million associated with

our closed block of long-term care insurance policies discussed further below. Amortization of deferred

acquisition costs included in operating costs was $55 million in 2013, $44 million in 2012, and $34 million in

2011.

Future policy benefits payable include $1.4 billion at December 31, 2013 and $1.1 billion at December 31,

2012 associated with a non-strategic closed block of long-term care insurance policies acquired in connection

with the 2007 acquisition of KMG. Future policy benefits payable includes amounts charged to accumulated

other comprehensive income for an additional liability that would exist on our closed-block of long-term care

insurance policies if unrealized gains on the sale of the investments backing such products had been realized and

the proceeds reinvested at then current yields. There was no additional liability at December 31, 2013 and $119

million of additional liability at December 31, 2012. Amounts charged to accumulated other comprehensive

income are net of applicable deferred taxes.

Long-term care insurance policies provide nursing home and home health coverage for which premiums are

collected many years in advance of benefits paid, if any. Therefore, our actual claims experience will emerge

many years after assumptions have been established. The risk of a deviation of the actual interest, morbidity,

mortality, and maintenance expense assumptions from those assumed in our reserves are particularly significant

to our closed block of long-term care insurance policies. We monitor the loss experience of these long-term care

insurance policies and, when necessary, apply for premium rate increases through a regulatory filing and

approval process in the jurisdictions in which such products were sold. To the extent premium rate increases and/

or loss experience vary from our loss recognition date assumptions, future adjustments to reserves could be

required.

131