Humana 2013 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2013 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

|

|

• Automatic across-the-board budget cuts under the Budget Control Act of 2011 and the American

Taxpayer Relief Act of 2012, known as “sequestration,” commenced in March 2013, including a 2%

reduction in Medicare Advantage and Medicare Part D payments beginning April 1, 2013. While we

believe we can reduce Medicare Advantage payments to providers under our network provider

contracts in connection with sequestration, a number of hospitals and other providers have asserted that

we are not entitled to do so, which have led and may lead to arbitration demands or other litigation

regarding these matters. While we believe our senior members’ benefits may be adversely impacted,

we believe we can effectively design Medicare Advantage products based upon these levels of rate

reduction while continuing to remain competitive compared to both the combination of original

Medicare with a supplement policy as well as Medicare Advantage products offered by our

competitors. Nonetheless, there can be no assurance that we will be able to successfully execute

operational and strategic initiatives that we have assumed when designing our plan benefit offerings

and premiums for 2014. Failure to execute these strategies may result in a material adverse effect on

our results of operations, financial position, and cash flows.

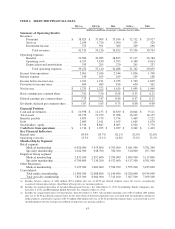

• For the year ended December 31, 2013, our Retail segment pretax income grew by 10.5%, primarily

driven by individual Medicare Advantage and Medicare stand-alone PDP membership growth in

excess of 7%.

• January 2014 individual Medicare Advantage membership increased approximately 250,000 members,

or 12%, from December 31, 2013. January 2014 Medicare stand-alone PDP membership, excluding the

LI-NET prescription drug plan program, increased approximately 500,000 members, or 16%, from

December 31, 2013. These increases reflect net membership additions for the 2014 enrollment season.

• Star Ratings issued by CMS in October 2013 indicated that 55% to 60% of our Medicare Advantage

members are now in plans with an overall Star Rating of four or more stars. We have 18 Medicare

Advantage plans that achieved a rating of four or more stars, an increase of 50% from the previous

year. We are offering nine Medicare Advantage plans that achieved a 4.5 Star Rating. Beginning in

2015, plans must have a Star Rating of four or higher to qualify for quality bonuses in the basic

premium rates.

• We were successful in our bids for state-based contracts in Florida and Virginia in 2013 and Ohio,

Illinois, and Kentucky in 2012. Ohio, Illinois, and Virginia are contracts for stand-alone dual eligible

demonstration programs serving individuals dually eligible for both the federal Medicare program and

the state-based Medicaid program. We partner with organizations, including CareSource Management

Group Company, to serve individuals in certain states. Medicaid membership in our Retail Segment at

December 31, 2013 increased 33,400 members from December 31, 2012, primarily driven by the

addition of our Kentucky Medicaid contract effective January 1, 2013 and Florida Long-Term Support

Services contracts in certain regions, including American Eldercare Inc. We expect to begin serving

new members in Ohio, Illinois, Virginia, and Florida at various dates between the first quarter and third

quarter of 2014. While we expect the Medicaid and dual-eligible demonstration business to result in

future growth, the mix of lower margin Medicaid and dual-eligible demonstration business with the

higher margin Medicare Advantage business may result in a decline in Retail segment margins over

time.

• On September 6, 2013, we acquired American Eldercare Inc., or American Eldercare, the largest

provider of nursing home diversion services in the state of Florida, serving frail and elderly individuals

in home and community-based settings. American Eldercare complements our core capabilities and

strength in serving seniors and disabled individuals with a unique focus on individualized and

integrated care, and has contracts to provide Medicaid long-term support services across the entire state

of Florida. The enrollment effective dates for the various regions range from August 2013 to March

2014.

• While we do not expect our quarterly earnings progression to be significantly different from our

recurring historical patterns, we do anticipate a slightly lower earnings run rate in the first half of 2014

due to the continuing administrative spending to support our state-based contracts.

47