Humana 2013 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2013 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

|

|

such that the liabilities established for IBNR have a greater probability of being adequate versus being

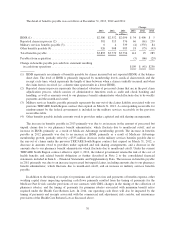

insufficient, or such that the liabilities established for IBNR are sufficient to cover obligations under an

assumption of moderately adverse conditions. Adverse conditions are situations in which the actual claims are

expected to be higher than the otherwise estimated value of such claims at the time of the estimate. Therefore, in

many situations, the claim amounts ultimately settled will be less than the estimate that satisfies the actuarial

standards of practice.

We develop our estimate for IBNR using actuarial methodologies and assumptions, primarily based upon

historical claim experience. Depending on the period for which incurred claims are estimated, we apply a

different method in determining our estimate. For periods prior to the most recent three months, the key

assumption used in estimating our IBNR is that the completion factor pattern remains consistent over a rolling

12-month period after adjusting for known changes in claim inventory levels and known changes in claim

payment processes. Completion factors result from the calculation of the percentage of claims incurred during a

given period that have historically been adjudicated as of the reporting period. For the most recent three months,

the incurred claims are estimated primarily from a trend analysis based upon per member per month claims

trends developed from our historical experience in the preceding months, adjusted for known changes in

estimates of recent hospital and drug utilization data, provider contracting changes, changes in benefit levels,

changes in member cost sharing, changes in medical management processes, product mix, and weekday

seasonality.

The completion factor method is used for the months of incurred claims prior to the most recent three

months because the historical percentage of claims processed for those months is at a level sufficient to produce a

consistently reliable result. Conversely, for the most recent three months of incurred claims, the volume of claims

processed historically is not at a level sufficient to produce a reliable result, which therefore requires us to

examine historical trend patterns as the primary method of evaluation. Changes in claim processes, including

recoveries of overpayments, receipt cycle times, claim inventory levels, outsourcing, system conversions, and

processing disruptions due to weather or other events affect views regarding the reasonable choice of completion

factors. Claim payments to providers for services rendered are often net of overpayment recoveries for claims

paid previously, as contractually allowed. Claim overpayment recoveries can result from many different factors,

including retroactive enrollment activity, audits of provider billings, and/or payment errors. Changes in patterns

of claim overpayment recoveries can be unpredictable and result in completion factor volatility, as they often

impact older dates of service. The receipt cycle time measures the average length of time between when a

medical claim was initially incurred and when the claim form was received. Increases in electronic claim

submissions from providers decrease the receipt cycle time. If claims are submitted or processed on a faster

(slower) pace than prior periods, the actual claim may be more (less) complete than originally estimated using

our completion factors, which may result in reserves that are higher (lower) than required.

Medical cost trends potentially are more volatile than other segments of the economy. The drivers of

medical cost trends include increases in the utilization of hospital facilities, physician services, new higher priced

technologies and medical procedures, and new prescription drugs and therapies, as well as the inflationary effect

on the cost per unit of each of these expense components. Other external factors such as government-mandated

benefits or other regulatory changes, the tort liability system, increases in medical services capacity, direct to

consumer advertising for prescription drugs and medical services, an aging population, lifestyle changes

including diet and smoking, catastrophes, and epidemics also may impact medical cost trends. Internal factors

such as system conversions, claims processing cycle times, changes in medical management practices and

changes in provider contracts also may impact our ability to accurately predict estimates of historical completion

factors or medical cost trends. All of these factors are considered in estimating IBNR and in estimating the per

member per month claims trend for purposes of determining the reserve for the most recent three months.

Additionally, we continually prepare and review follow-up studies to assess the reasonableness of the estimates

generated by our process and methods over time. The results of these studies are also considered in determining

the reserve for the most recent three months. Each of these factors requires significant judgment by management.

76