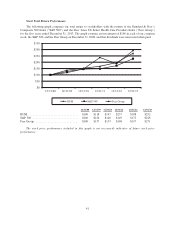

Humana 2013 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2013 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

|

|

year preceding payment, beginning in 2014. Accordingly, in addition to recording the full-year 2014

assessment in the first quarter of 2014, we may be required to restrict surplus for the 2015 assessment

ratably in 2014. Accordingly, dividends from the subsidiaries to the parent in 2014 could be reduced. In

2014, we expect to pay the federal government in the range of $525 million to $575 million for the

annual health insurance industry fee. In 2015, the health insurance industry fee increases by 41% for

the industry taken as a whole. Accordingly, absent changes in market share, we would expect a similar

increase in our fee in 2015.

The Health Care Reform Law also specifies benefit design guidelines, limits rating and pricing practices,

encourages additional competition from the establishment of two multi-state plans (one not-for-profit; one for-

profit) administered through the Office of Personnel Management, and expands eligibility for Medicaid

programs. In addition, the Health Care Reform Law has increased and will continue to increase federal oversight

of health plan premium rates and could adversely affect our ability to appropriately adjust health plan premiums

on a timely basis. Financing for these reforms will come, in part, from material additional fees and taxes on us

(as discussed above) and other health plans and individuals beginning in 2014, as well as reductions in certain

levels of payments to us and other health plans under Medicare as described in this report.

As discussed above, implementing regulations and related interpretive guidance continue to be issued on

certain provisions of the Health Care Reform Law. Given the breadth of possible changes and the uncertainties of

interpretation, implementation, and timing of these changes, the Health Care Reform Law will change the way

we do business, potentially impacting our pricing, benefit design, product mix, geographic mix, and distribution

channels. The response of other companies to the Health Care Reform Law and adjustments to their offerings, if

any, could cause meaningful disruption in local health care markets. It is reasonably possible that the Health Care

Reform Law and related regulations, as well as future legislative changes, including legislative restrictions on our

ability to manage our provider network, in the aggregate may have a material adverse effect on our results of

operations (including restricting revenue, enrollment and premium growth in certain products and market

segments, restricting our ability to expand into new markets, increasing our medical and operating costs, further

lowering our Medicare payment rates and increasing our expenses associated with the non-deductible health

insurance industry fee and other assessments); our financial position (including our ability to maintain the value

of our goodwill); and our cash flows (including the receipt of amounts due under the commercial risk adjustment,

risk corridor, and reinsurance provisions of the Health Care Reform Law in 2015 related to claims paid in 2014).

If we are unable to adjust our business model to address the non-deductible health insurance industry fee and

other assessments, including the three-year commercial reinsurance fee, such as through the reduction of our

operating costs or adjustments to premium pricing or benefit design, there can be no assurance that the non-

deductible health insurance industry fee and other assessments would not have a material adverse effect on our

results of operations, financial position, and cash flows.

We intend for the discussion of our financial condition and results of operations that follows to assist in the

understanding of our financial statements and related changes in certain key items in those financial statements

from year to year, including the primary factors that accounted for those changes. Transactions between

reportable segments consist of sales of services rendered by our Healthcare Services segment, primarily

pharmacy, provider, and behavioral health services, to our Retail and Employer Group customers and are

described in Note 16 to the consolidated financial statements included in Item 8. – Financial Statements and

Supplementary Data.

51