Toyota 2013 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2013 Toyota annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

Toyota Global Vision President’s Message Launching a New Structure Special Feature Review of Operations

Consolidated Performance

Highlights

Management and

Corporate Information Investor InformationFinancial Section

Page 66

NextPrev

ContentsSearchPrint

ANNUAL REPORT 2013

Credit Facilities with Dealers

Toyota’s fi nancial services operations maintain credit

facilities with dealers. These credit facilities may be

used for business acquisitions, facilities refurbish-

ment, real estate purchases, and working capital

requirements. These loans are typically collateralized

with liens on real estate, vehicle inventory, and/or

other dealership assets, as appropriate. Toyota

obtains a personal guarantee from the dealer or

corporate guarantee from the dealership when

deemed prudent. Although the loans are typically

collateralized or guaranteed, the value of the under-

lying collateral or guarantees may not be suffi cient

to cover Toyota’s exposure under such agreements.

Toyota prices the credit facilities according to the

risks assumed in entering into the credit facility.

Toyota’s fi nancial services operations also provide

fi nancing to various multi-franchise dealer organiza-

tions, referred to as dealer groups, often as part of

a lending consortium, for wholesale inventory fi nancing,

business acquisitions, facilities refurbishment, real

estate purchases, and working capital requirements.

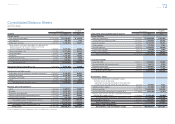

Toyota’s outstanding credit facilities with dealers

totaled ¥1,795.8 billion as of March 31, 2013.

Guarantees

Toyota enters into certain guarantee contracts with

its dealers to guarantee customers’ payments of

their installment payables that arise from installment

contracts between customers and Toyota dealers,

as and when requested by Toyota dealers.

Guarantee periods are set to match the maturity of

installment payments, and as of March 31, 2013,

ranged from one month to 35 years. However, they

are generally shorter than the useful lives of prod-

ucts sold. Toyota is required to execute its guaran-

tee primarily when customers are unable to make

required payments.

The maximum potential amount of future pay-

ments as of March 31, 2013 is ¥1,849.4 billion.

Liabilities for these guarantees of ¥6.5 billion have

been provided as of March 31, 2013. Under these

guarantee contracts, Toyota is entitled to recover

any amounts paid by it from the customers whose

obligations it guaranteed.

Toyota uses its securitization program as part of its

funding through special purpose entities for its

fi nancial services operations. Toyota is considered

the primary benefi ciary of these special purpose

entities and therefore consolidates them. Toyota has

not entered into any off-balance sheet securitization

transactions during fi scal 2013.

Off-Balance Sheet Arrangements

Credit Facilities with Credit Card Holders

Toyota’s fi nancial services operations issue credit

cards to customers. As customary for credit card

businesses, Toyota maintains credit facilities with

holders of credit cards issued by Toyota. These

facilities are used upon each holder’s requests up to

the limits established on an individual holder’s basis.

Although loans made to customers through these

facilities are not secured, for the purposes of

Lending Commitments

minimizing credit risks and of appropriately estab-

lishing credit limits for each individual credit card

holder, Toyota employs its own risk management

policy which includes an analysis of information pro-

vided by fi nancial institutions in alliance with Toyota.

Toyota periodically reviews and revises, as appropri-

ate, these credit limits. Outstanding credit facilities

with credit card holders were ¥245.2 billion as of

March 31, 2013.

For information regarding debt obligations, capital

lease obligations, operating lease obligations and

other obligations, including amounts maturing in

each of the next fi ve years, see notes 13, 22 and 23

to the consolidated fi nancial statements. In addition,

as part of Toyota’s normal business practices,

Toyota enters into long-term arrangements with

suppliers for purchases of certain raw materials,

components and services. These arrangements

may contain fi xed/minimum quantity purchase

requirements. Toyota enters into such arrangements

to facilitate an adequate supply of these materials

and services.

Contractual Obligations and Commitments

Management’s Discussion and Analysis of Financial Condition and Results of Operations

pension benefi t obligations resulted from a decline

in discount rate. On the other hand, the increase in

liabilities of foreign plans refl ects the increase in

pension benefi t obligations resulted from a decline

in discount rate. See note 19 to the consolidated

fi nancial statements for further discussion.

Toyota’s treasury policy is to maintain controls on

all exposures, to adhere to stringent counterparty credit

standards, and to actively monitor marketplace

exposures. Toyota remains centralized, and is pur-

suing global effi ciency of its fi nancial services opera-

tions through Toyota Financial Services Corporation.

The key element of Toyota’s fi nancial strategy is

maintaining a strong fi nancial position that will allow

Toyota to fund its research and development

initiatives, capital expenditures and fi nancial services

operations effi ciently even if earnings are subject to

short-term fl uctuations. Toyota believes that it main-

tains suffi cient liquidity for its present requirements

and that by maintaining its high credit ratings, it will

continue to be able to access funds from external

sources in large amounts and at relatively low costs.

Toyota’s ability to maintain its high credit ratings is

subject to a number of factors, some of which are

not within Toyota’s control. These factors include

general economic conditions in Japan and the other

major markets in which Toyota does business, as

well as Toyota’s successful implementation of its

business strategy.

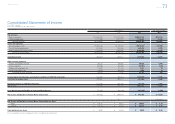

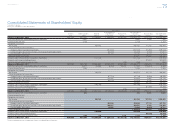

Selected Financial Summary (U.S. GAAP) Consolidated Segment Information Consolidated Quarterly Financial Summary Management’s Discussion and Analysis of Financial Condition and Results of Operations [21 of 26] Consolidated Financial Statements Notes to Consolidated Financial Statements

Management’s Annual Report on Internal Control over Financial Reporting Report of Independent Registered Public Accounting Firm