Toyota 2013 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2013 Toyota annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

|

|

Toyota Global Vision President’s Message Launching a New Structure Special Feature Review of Operations

Consolidated Performance

Highlights

Management and

Corporate Information Investor InformationFinancial Section

Page 81

NextPrev

ContentsSearchPrint

ANNUAL REPORT 2013

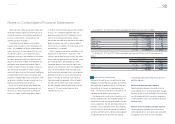

Reserve rates are calculated mainly by historical loss

experience, current economic events and conditions

and other pertinent factors such as used car markets.

Wholesale and other dealer loan

receivables portfolio segment

Toyota calculates allowance for credit losses to

cover probable losses on wholesale and other deal-

er loan receivables by applying reserve rates to such

receivables. Reserve rates are calculated mainly by

fi nancial conditions of the dealers, terms of collateral

setting, current economic events and conditions

and other pertinent factors.

Toyota establishes specifi c reserves to cover the

estimated losses on individually impaired receivables

within the wholesale and other dealer loan receiv-

ables portfolio segment. Specifi c reserves on

impaired receivables are determined by the present

value of expected future cash fl ows or the fair value

of collateral when it is probable that such receiv-

ables will be unable to be fully collected. The fair

value of the underlying collateral is used if the receiv-

able is collateral-dependent. The receivable is deter-

mined collateral-dependent if the repayment of the

loan is expected to be provided by the underlying

collateral. For the receivables in which the fair value

of the underlying collateral was in excess of the out-

standing balance, no allowance was provided.

Troubled debt restructurings in the retail receiv-

ables and fi nance lease receivables portfolio seg-

ments are specifi cally identifi ed as impaired and

aggregated with their respective portfolio segments

when determining the allowance for credit losses.

Impaired loans in the retail receivables and fi nance

levels to determine whether reserves are considered

adequate to cover the probable range of losses.

The allowance for residual value losses is main-

tained in amounts considered by Toyota to be

appropriate in relation to the estimated losses on its

owned portfolio. Upon disposal of the assets, the

allowance for residual losses is adjusted for the dif-

ference between the net book value and the pro-

ceeds from sale.

Inventories

Inventories are valued at cost, not in excess of mar-

ket, cost being determined on the “average-cost”

basis, except for the cost of fi

nished products car-

ried by certain subsidiary companies which is deter-

mined on the “specifi c identifi cation” basis or

“last-in, fi rst-out” (“LIFO”) basis. Inventories valued

on the LIFO basis totaled ¥220,582 million and

¥220,082 million ($2,340 million) at March 31, 2012

and 2013, respectively. Had the “fi rst-in, fi rst-out”

basis been used for those companies using the

LIFO basis, inventories would have been ¥56,799

million and ¥66,979 million ($712 million) higher than

reported at March 31, 2012 and 2013, respectively.

Property, plant and equipment

Property, plant and equipment are stated at cost.

Major renewals and improvements are capitalized;

minor replacements, maintenance and repairs are

charged to current operations. Depreciation of

property, plant and equipment is mainly computed

on the declining-balance method for the parent

company and Japanese subsidiaries and on the

straight-line method for foreign subsidiary companies

lease receivables portfolio segments are insignifi cant

for individual evaluation and Toyota has determined

that allowance for credit losses for each of the retail

receivables and fi nance lease receivables portfolio

segments would not be materially different if they

had been individually evaluated for impairment.

Specifi c reserves on impaired receivables within

the wholesale and other dealer loan receivables

portfolio segment are recorded by an increase to

the allowance for credit losses based on the related

measurement of impairment. Related collateral, if

recoverable, is repossessed and sold and the

account balance is written-off.

Any shortfall between proceeds received and the

carrying cost of repossessed collateral is charged to

the allowance. Recoveries are reversed from the

allowance for credit losses.

Allowance for residual value losses

Toyota is exposed to risk of loss on the disposition

of off-lease vehicles to the extent that sales proceeds

are not suffi cient to cover the carrying value of the

leased asset at lease termination. Toyota maintains

an allowance to cover probable estimated losses

related to unguaranteed residual values on its owned

portfolio. The allowance is evaluated considering

projected vehicle return rates and projected loss

severity. Factors considered in the determination of

projected return rates and loss severity include his-

torical and market information on used vehicle

sales, trends in lease returns and new car markets,

and general economic conditions. Management

evaluates the foregoing factors, develops several

potential loss scenarios, and reviews allowance

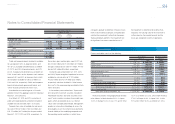

at rates based on estimated useful lives of the

respective assets according to general class, type

of construction and use. The estimated useful lives

range from 2 to 65 years for buildings and from 2 to

20 years for machinery and equipment.

Vehicles and equipment on operating leases to

third parties are originated by dealers and acquired

by certain consolidated subsidiaries. Such subsid-

iaries are also the lessors of certain property that

they acquire directly. Vehicles and equipment on

operating leases are depreciated primarily on a

straight-line method over the lease term, generally

from 2 to 5 years, to the estimated residual value.

Incremental direct costs incurred in connection with

the acquisition of operating lease contracts are cap-

italized and amortized on a straight-line method

over the lease term.

Long-lived assets

Toyota reviews its long-lived assets for impairment

whenever events or changes in circumstances indi-

cate that the carrying amount of an asset group

may not be recoverable. An impairment loss would

be recognized when the carrying amount of an

asset group exceeds the estimated undiscounted

cash fl ows expected to result from the use of the

asset and its eventual disposition. The amount of

the impairment loss to be recorded is calculated by

the excess of the carrying value of the asset group

over its fair value. Fair value is determined mainly

using a discounted cash fl ow valuation method.

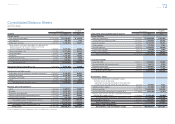

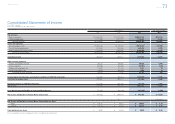

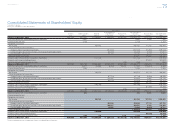

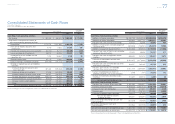

Notes to Consolidated Financial Statements

Selected Financial Summary (U.S. GAAP) Consolidated Segment Information Consolidated Quarterly Financial Summary Management’s Discussion and Analysis of Financial Condition and Results of Operations Consolidated Financial Statements Notes to Consolidated Financial Statements [4 of 44]

Management’s Annual Report on Internal Control over Financial Reporting Report of Independent Registered Public Accounting Firm