Electronic Arts 2014 Annual Report Download - page 128

Download and view the complete annual report

Please find page 128 of the 2014 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

|

|

We believe the counterparties to these foreign currency forward and option contracts are creditworthy

multinational commercial banks. While we believe the risk of counterparty nonperformance is not material, a

sustained decline in the financial stability of financial institutions as a result of disruption in the financial markets

could affect our ability to secure credit-worthy counterparties for our foreign currency hedging programs.

Notwithstanding our efforts to mitigate some foreign currency exchange rate risks, there can be no assurance that

our hedging activities will adequately protect us against the risks associated with foreign currency fluctuations.

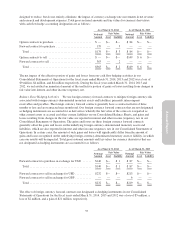

As of March 31, 2014, a hypothetical adverse foreign currency exchange rate movement of 10 percent or 20

percent would have resulted in potential declines in the fair value of the premiums on our foreign currency

forward and option contracts used in cash flow hedging of $54 million and $108 million, respectively. As of

March 31, 2014, a hypothetical adverse foreign currency exchange rate movement of 10 percent or 20 percent

would have resulted in potential losses on our foreign currency forward contracts used in balance sheet hedging

of $37 million and $74 million, respectively. This sensitivity analysis assumes an adverse shift of all foreign

currency exchange rates; however, all foreign currency exchange rates do not always move in such manner and

actual results may differ materially.

Interest Rate Risk

Our exposure to market risk for changes in interest rates relates primarily to our short-term investment portfolio.

We manage our interest rate risk by maintaining an investment portfolio generally consisting of debt instruments

of high credit quality and relatively short maturities. However, because short-term investments mature relatively

quickly and are required to be reinvested at the then-current market rates, interest income on a portfolio

consisting of short-term investments is more subject to market fluctuations than a portfolio of longer term

investments. Additionally, the contractual terms of the investments do not permit the issuer to call, prepay or

otherwise settle the investments at prices less than the stated par value. Our investments are held for purposes

other than trading. Also, we do not use derivative financial instruments in our short-term investment portfolio.

As of March 31, 2014 and 2013, our short-term investments were classified as available-for-sale securities and,

consequently, were recorded at fair market value with unrealized gains or losses resulting from changes in fair

value reported as a separate component of accumulated other comprehensive income, net of tax, in stockholders’

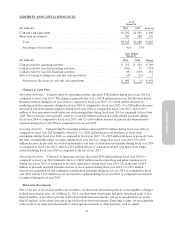

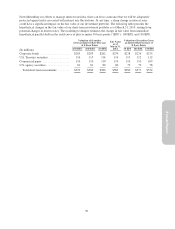

equity. Our portfolio of short-term investments consisted of the following investment categories, summarized by

fair value as of March 31, 2014 and 2013 (in millions):

As of March 31,

2014 2013

Corporate bonds ........................................................... $279 $178

U.S. Treasury securities ..................................................... 114 85

Commercial paper ......................................................... 110 49

U.S. agency securities ...................................................... 80 76

Total short-term investments ............................................... $583 $388

58