Electronic Arts 2014 Annual Report Download - page 143

Download and view the complete annual report

Please find page 143 of the 2014 Electronic Arts annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

|

|

Annual Report

involves assumptions about future activity. Certain taxable temporary differences that are not expected to reverse

during the carry forward periods permitted by tax law cannot be considered as a source of future taxable income

that may be available to realize the benefit of deferred tax assets.

Based on the assumptions and requirements noted above, we have recorded a valuation allowance against most of

our U.S. deferred tax assets. In addition, we expect to provide a valuation allowance on future U.S. tax benefits

until we can sustain a level of profitability in the U.S., or until other significant positive evidence arises that

suggest that these benefits are more likely than not to be realized.

Impact of Recently Issued Accounting Standards

In April 2014, the FASB issued ASU 2014-08, Presentation of Financial Statements (Topic 205) and Property,

Plant, and Equipment (Topic 360). The amendments of this ASU require that only the disposals representing a

strategic shift in operations should be presented as discontinued operations. Those strategic shifts should have a

major effect on the organization’s operations and financial results. The disclosure requirements will be effective

for annual periods (and interim periods within those annual periods) beginning after December 15, 2014, and will

require prospective application. Early adoption is permitted. We expect to adopt this new standard in the first

quarter of fiscal year 2016. We do not expect the adoption to have a material impact on our Consolidated

Financial Statements.

In July 2013, the FASB issued ASU 2013-11, Income Taxes (Topic 220): Presentation of an Unrecognized Tax

Benefit When a Net Operating Loss Carryforward, a Similar Tax Loss, or a Tax Credit Carryforward Exists. The

amendments of this ASU require that entities that have an unrecognized tax benefit and a net operating loss

carryforward or similar tax loss or tax credit carryforward in the same jurisdiction as the uncertain tax position

present the unrecognized tax benefit as a reduction of the deferred tax asset for the loss or tax credit carryforward

rather than as a liability when the uncertain tax position would reduce the loss or tax credit carryforward under

the tax law. The disclosure requirements will be effective for annual periods (and interim periods within those

annual periods) beginning after December 15, 2013, and will require prospective application. Early adoption is

permitted. The adoption will impact our balance sheet only, and we expect to adopt this new standard in the first

quarter of fiscal year 2015. While we have not completed our analysis, we anticipate the adoption will result in

equal reductions to both deferred tax assets and noncurrent income tax obligations between $80 million and $90

million.

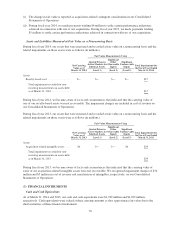

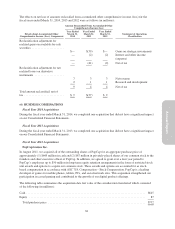

(2) FAIR VALUE MEASUREMENTS

There are various valuation techniques used to estimate fair value, the primary one being the price that would be

received from selling an asset or paid to transfer a liability in an orderly transaction between market participants

at the measurement date. When determining fair value, we consider the principal or most advantageous market in

which we would transact and consider assumptions that market participants would use when pricing the asset or

liability. We measure certain financial and nonfinancial assets and liabilities at fair value on a recurring and

nonrecurring basis.

Fair Value Hierarchy

The three levels of inputs that may be used to measure fair value are as follows:

•Level 1. Quoted prices in active markets for identical assets or liabilities.

•Level 2. Observable inputs other than quoted prices included within Level 1, such as quoted prices for

similar assets or liabilities, quoted prices in markets with insufficient volume or infrequent transactions

(less active markets), or model-derived valuations in which all significant inputs are observable or can be

derived principally from or corroborated with observable market data for substantially the full term of the

assets or liabilities.

•Level 3. Unobservable inputs to the valuation methodology that are significant to the measurement of the

fair value of assets or liabilities.

73