BB&T 2007 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2007 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

BB&T CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

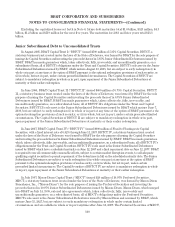

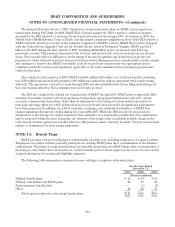

The Internal Revenue Service (“IRS”) disallowed certain deductions taken by BB&T on leveraged lease

transactions during 1997-2002. In 2004, BB&T filed a lawsuit against the IRS to pursue a refund of amounts

assessed by the IRS related to a leveraged lease transaction entered into during 1997. On January 4, 2007, the

United States Middle District Court of North Carolina issued a summary judgment in favor of the IRS related to

BB&T’s lawsuit. Based on a review of the summary judgment by BB&T’s counsel, BB&T filed a notice of appeal

with the United States Appeals Court for the Fourth Circuit, based in Richmond, Virginia. BB&T paid $1.2

billion to the IRS during the first quarter of 2007, including $284 million in pre-tax interest that had been

previously accrued. This payment represented the total tax and interest due on these transactions for all open

years. The tax paid relates to differences in the timing of income recognition and deductions for income tax

purposes for which deferred taxes had been previously provided. Management has consulted with outside counsel

and continues to believe that BB&T’s treatment of its leveraged lease transactions was appropriate and in

compliance with the tax laws and regulations applicable to the years examined and is pursuing legal remedies

related to this issue.

Also, during the first quarter of 2007, BB&T paid $48 million ($32 million, net of federal benefit), including

tax of $39 million and interest and penalties of $9 million in conjunction with an agreement with a state taxing

authority. The agreement covered tax years through 2005 and also established the future filing methodology for

that state taxing authority. These amounts were previously accrued.

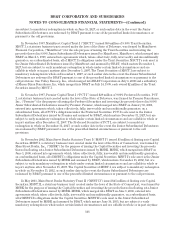

The IRS has completed its federal tax examinations of BB&T through 2005. BB&T plans to appeal the IRS’

assertion of penalties related to its leveraged lease transactions and proposed deficiencies related to certain

executive compensation deductions. Other than an adjustment to the timing of certain deductions related to

mortgage servicing rights for which deferred taxes have previously been provided, no significant adjustments

have been proposed. In addition, the IRS is currently examining a deconsolidated subsidiary of BB&T that

claimed significant foreign tax credits during tax years 2002-2007. While the IRS has not yet proposed any

adjustments to the foreign tax credits claimed by this subsidiary, it is reasonably possible that such adjustments

may be proposed within the next 12 months. An estimate of the range of the reasonably possible change in the

total amount of unrecognized tax benefits related to this position cannot currently be made. Various years remain

subject to examination by state taxing authorities.

NOTE 14. Benefit Plans

BB&T provides various benefit plans to substantially all employees, including employees of acquired entities.

Employees of acquired entities generally participate in existing BB&T plans after consummation of the business

combinations. The plans of acquired institutions are typically merged into the BB&T plans after consummation of

the mergers, and, under these circumstances, credit is usually given to these employees for years of service at the

acquired institution for vesting and eligibility purposes.

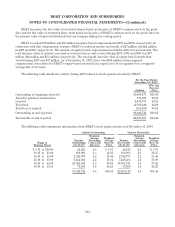

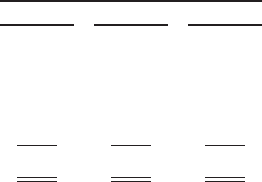

The following table summarizes expenses (income) relating to employee retirement plans:

For the Years Ended

December 31,

2007 2006 2005

(Dollars in millions)

Defined benefit plans $ 32 $ 50 $ 43

Defined contribution and ESOP plans 72 67 59

Postretirement benefit plans — (1) (3)

Other 12 20 11

Total expense related to retirement benefit plans $116 $136 $110

108