BB&T 2007 Annual Report Download - page 58

Download and view the complete annual report

Please find page 58 of the 2007 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

instruments, changes in market conditions, loan volumes and pricing, deposit sensitivity, customer preferences

and capital plans. The resulting change in interest sensitive income reflects the level of sensitivity that interest

sensitive income has in relation to changing interest rates.

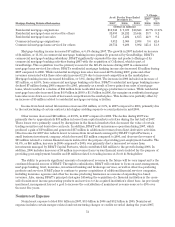

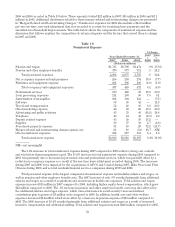

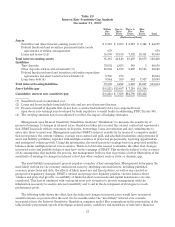

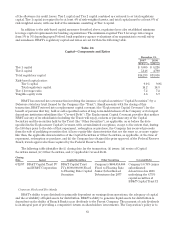

Table 21

Interest Sensitivity Simulation Analysis

Interest Rate Scenario Annualized Hypothetical

Percentage Change in Net Interest Income

Linear

Change in

Prime Rate

Prime Rate

December 31, December 31,

2007 2006 2007 2006

3.00% 10.25% 11.25% (3.15)% (3.12)%

1.50 8.75 9.75 (2.19) (2.19)

No Change 7.25 8.25 — —

(1.50) 5.75 6.75 0.44 1.58

(3.00) 4.25 5.25 1.29 1.96

Management has established parameters for asset/liability management, which prescribe a maximum

negative impact on interest sensitive income of 3% for the next 12 months for a linear increase of 150 basis points

for six months followed by a flat interest rate scenario for the remaining six month period, and a maximum

negative impact of 6% for a linear increase of 300 basis points for 12 months.

Liquidity

Liquidity represents BB&T’s continuing ability to meet funding needs, primarily deposit withdrawals, timely

repayment of borrowings and other liabilities, and funding of loan commitments. In addition to the level of liquid

assets, such as trading securities and securities available for sale, many other factors affect the ability to meet

liquidity needs, including access to a variety of funding sources, maintaining borrowing capacity in national

money markets, growing core deposits, the repayment of loans and the capability to securitize or package loans

for sale.

The purpose of BB&T Corporation (the “Parent Company”) is to serve as the capital financing vehicle for the

operating subsidiaries. The assets of the Parent Company consist primarily of cash on deposit with Branch Bank,

equity investments in subsidiaries, advances to subsidiaries, accounts receivable from subsidiaries, and other

miscellaneous assets. The principal obligations of the Parent Company are principal and interest on master notes,

long-term debt, and redeemable capital securities. The main sources of funds for the Parent Company are

dividends and management fees from subsidiaries, repayments of advances to subsidiaries, and proceeds from

issuance of long-term debt and master notes. The primary uses of funds by the Parent Company are for the

retirement of common stock, investments in subsidiaries, advances to subsidiaries, dividend payments to

shareholders, and interest and principal payments due on long-term debt and master notes.

The primary source of funds used for Parent Company cash requirements has been dividends declared from

Branch Bank, which totaled $1.2 billion during 2007, and net proceeds from the issuance of long-term debt, which

totaled $350 million in 2007. Funds raised through master note agreements with commercial clients are placed in

a note receivable at Branch Bank primarily for its use in meeting short-term funding needs and, to a lesser

extent, to support the short-term temporary cash needs of the Parent Company. At December 31, 2007 and 2006,

master note balances totaled $1.8 billion and $1.4 billion, respectively.

During 2005, BB&T filed a universal shelf registration statement with the Securities and Exchange

Commission to provide for the issuance of up to $2.5 billion of securities, which could include unsecured debt

securities, shares of common stock, shares of preferred stock, depositary shares representing fractional interest

in preferred stock, stock purchase contracts, stock purchase units, warrants to purchase debt securities,

preferred stock or common stock, or units consisting of a combination of these securities. In addition, the

58