BB&T 2007 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2007 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

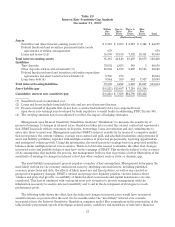

The liabilities for severance and personnel-related costs relate to severance liabilities that will be paid out

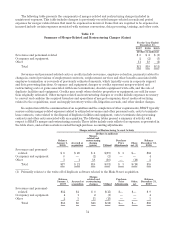

based on such factors as expected termination dates, the provisions of employment contracts and the terms of

BB&T’s severance plans. The remaining occupancy and equipment accruals relate to costs to exit certain leases

and to dispose of excess facilities and equipment. Such liabilities will be utilized upon termination of the various

leases and sale of duplicate property.

In general, a major portion of accrued costs are utilized in conjunction with or immediately following the

systems conversion, when most of the duplicate positions are eliminated and the terminated employees begin to

receive severance. Other accruals are utilized over time based on the sale, closing or disposal of duplicate facilities

or equipment or the expiration of lease contracts. Merger accruals are re-evaluated periodically and adjusted as

necessary. The remaining accruals at December 31, 2007 are expected to be utilized during 2008, unless they

relate to specific contracts that expire in later years.

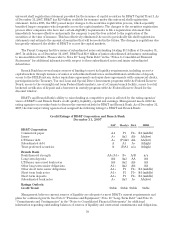

Provision for Income Taxes

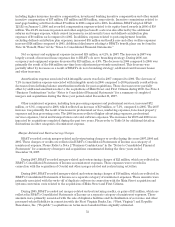

BB&T’s provision for income taxes totaled $836 million for 2007, a decrease of $109 million, or 11.5%,

compared to 2006. The provisions for income taxes totaled $945 million in 2006 and $813 million in 2005. BB&T’s

effective tax rates for the years ended 2007, 2006 and 2005 were 32.5%, 38.2%, and 33.0%, respectively. In 2006,

the higher provision for income taxes and the higher effective tax rate were primarily the result of an adjustment

of $139 million to BB&T’s tax reserves for leveraged lease transactions as discussed below. A reconciliation of the

effective tax rate to the statutory tax rate is included in Note 13 “Income Taxes” in the “Notes to Consolidated

Financial Statements” herein.

BB&T has extended credit to, and invested in, the obligations of states and municipalities and their agencies,

and has made other investments and loans that produce tax-exempt income. The income generated from these

investments together with certain other transactions that have favorable tax treatment have reduced BB&T’s

overall effective tax rate from the statutory rate in 2007, 2006 and 2005.

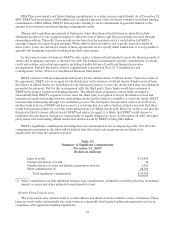

BB&T continually monitors and evaluates the potential impact of current events and circumstances on the

estimates and assumptions used in the analysis of its income tax positions and, accordingly, BB&T’s effective tax

rate may fluctuate in the future. On a periodic basis, BB&T evaluates its income tax positions based on tax laws

and regulations and financial reporting considerations, and records adjustments as appropriate. This evaluation

takes into consideration the status of current taxing authorities’ examinations of BB&T’s tax returns, recent

positions taken by the taxing authorities on similar transactions, if any, and the overall tax environment in

relation to tax-advantaged transactions. Accordingly, the results of these examinations may alter the timing or

amount of taxable income or deductions or the allocation of income among tax jurisdictions. In this regard, the

Internal Revenue Service (“IRS”) disallowed certain deductions taken by BB&T on leveraged lease transactions

during 1997-2002. In 2004, BB&T filed a lawsuit against the IRS to pursue a refund of amounts assessed by the

IRS related to a leveraged lease transaction entered into during 1997. On January 4, 2007, the United States

Middle District Court of North Carolina issued a summary judgment in favor of the IRS related to BB&T’s

lawsuit. Based on a review of the summary judgment by BB&T’s counsel, BB&T filed a notice of appeal with the

United States Appeals Court for the Fourth Circuit, based in Richmond, Virginia.

Due to the timing of the District Court’s ruling and its potential impact on BB&T’s other leveraged lease

transactions, BB&T recorded $139 million in additional reserves in the fourth quarter of 2006 and paid $1.2 billion

to the IRS during the first quarter of 2007. This payment represented the total tax and interest due on these

transactions for all open years. The tax paid relates to differences in the timing of income recognition and

deductions for income tax purposes for which deferred taxes had been previously provided.

Management has consulted with outside counsel and continues to believe that BB&T’s treatment of its

leveraged lease transactions was appropriate and in compliance with the tax laws and regulations applicable to

the years examined.

Market Risk Management

The effective management of market risk is essential to achieving BB&T’s strategic financial objectives. As a

financial institution, BB&T’s most significant market risk exposure is interest rate risk; however, market risk

55