BB&T 2007 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2007 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

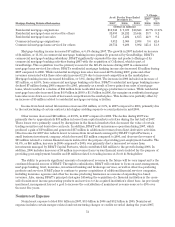

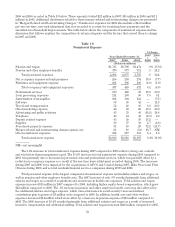

direct retail loans to lower-yielding mortgage loans and commercial and industrial loans. Second, higher levels of

nonaccruals have negatively affected net interest income and the net interest margin. Third, increased liability

costs, specifically a shift to higher-cost deposits from lower-cost transaction accounts, contributed to the margin

compression. The decline in the net interest margin during 2006 compared to 2005 was due to a faster increase in

the cost of funds compared to interest-earning assets. This was primarily a result of a delay in the repricing of

earning assets compared to interest-bearing liabilities and a change in the mix of funding sources with a higher

concentration of deposits in higher-cost products. In addition to the lag effect described above, the margin was

also negatively affected by a flat yield curve during 2005, which became inverted in 2006. The inverted yield

curve is a significant challenge for financial services companies, like BB&T, who borrow money from clients in the

form of deposits and pay short-term rates, and invest in assets with longer-term maturities, which generally

produce an interest spread. BB&T’s net interest margin in 2006 and 2007 was also negatively impacted by the

additional interest expense incurred in connection with BB&T’s share repurchase program.

46