BB&T 2007 Annual Report Download - page 49

Download and view the complete annual report

Please find page 49 of the 2007 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

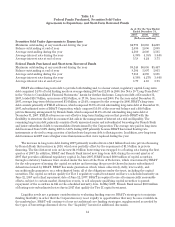

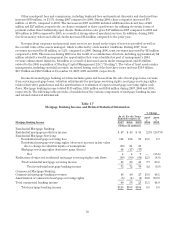

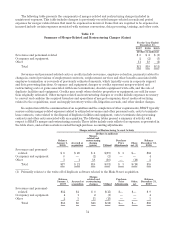

The following table provides a breakdown of BB&T’s noninterest income:

Table 16

Noninterest Income

% Change

Years Ended December 31, 2007

v.

2006

2006

v.

20052007 2006 2005

(Dollars in millions)

Insurance commissions $ 853 $ 813 $ 714 4.9% 13.9%

Service charges on deposits 611 548 543 11.5 .9

Investment banking and brokerage fees and commissions 343 317 290 8.2 9.3

Other nondeposit fees and commissions 184 167 129 10.2 29.5

Check card fees 180 155 128 16.1 21.1

Trust income 162 154 141 5.2 9.2

Bankcard fees and merchant discounts 139 122 112 13.9 8.9

Mortgage banking income 115 108 104 6.5 3.8

Securities losses, net (3) (73) — NM NM

Income from bank-owned life insurance 101 93 94 8.6 (1.1)

Other noninterest income 89 117 71 (23.9) 64.8

Total noninterest income $2,774 $2,521 $2,326 10.0% 8.4%

NM—not meaningful

The 10.0% growth in noninterest income was the result of increased revenues from essentially all of BB&T’s

fee-based businesses during 2007. These increases were partially offset by trading losses at Scott & Stringfellow.

The 8.4% growth in noninterest income for 2006 was the result of increased revenues from all of BB&T’s major

fee-based businesses. These increases were partially offset by a loss from sales of securities as a result of

management’s decision to restructure a portion of the securities portfolio during the fourth quarter of 2006, and a

slight decline in income from bank-owned life insurance. The major categories of noninterest income and fluctuations

in these amounts are discussed in the following paragraphs. These fluctuations reflect the impact of acquisitions.

Revenues from BB&T’s insurance agency/brokerage operations were the largest source of noninterest

income. Internal growth, combined with the expansion of BB&T’s insurance agency network through acquisitions

during the last two years, resulted in growth of 4.9% in 2007 and 13.9% in 2006. The increase in insurance

commissions in 2007 compared to 2006 was primarily related to the sale of property and casualty, and employee

benefit insurance, which increased $17.0 million and $9.1 million, respectively. These increases were the result of

strong new sales of products, which was partially offset by more competitive pricing in the property and casualty

insurance market. The increase in commission income during 2006 included increases in property and casualty

insurance and employee benefit-related insurance commissions of $77 million and $10 million, respectively,

compared to 2005.

Service charges on deposit accounts represent BB&T’s second largest category of noninterest revenue.

Service charge revenue increased $63 million, or 11.5%, compared to 2006. Service charge revenue grew primarily

due to strong transaction account growth and increased revenue from overdraft items. Service charge revenue

was up slightly during 2006, primarily due to management’s decision to offer more free services as a method of

attracting and retaining clients. The resulting decline caused by these changes in pricing strategy was more than

offset by an increase of $24 million on higher revenues from overdraft items in 2006 compared to 2005.

Investment banking and brokerage fees and commissions increased $26 million, or 8.2%, compared to 2006

primarily as a result of increased revenues of $20 million at Scott & Stringfellow, BB&T’s full-service brokerage

and investment banking subsidiary. The remainder of the increase was generated by BB&T Investment Services,

Inc. The 9.3% increase in 2006 compared to 2005 resulted primarily from growth in investment banking and retail

brokerage revenues of $23 million at Scott & Stringfellow, and was aided by the acquisition of Bergen Capital,

Inc., which was completed in January 2006.

49