BB&T 2007 Annual Report Download - page 83

Download and view the complete annual report

Please find page 83 of the 2007 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

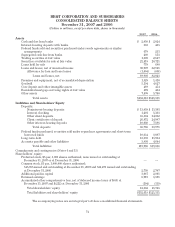

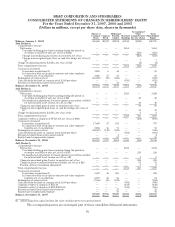

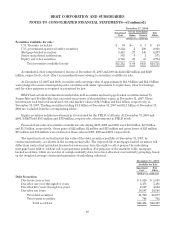

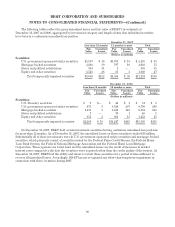

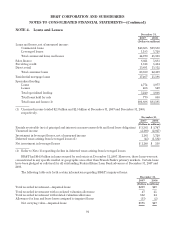

BB&T CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

Derivative Financial Instruments

A derivative is a financial instrument that derives its cash flows, and therefore its value, by reference to an

underlying instrument, index or referenced interest rate. These instruments include interest rate swaps, caps,

floors, collars, financial forwards and futures contracts, swaptions, when-issued securities, foreign exchange

contracts and options written and purchased. BB&T uses derivatives primarily to manage economic risk related

to securities, business loans, mortgage servicing rights and mortgage banking operations, Federal funds

purchased, other time deposits, long-term debt and institutional certificates of deposit. BB&T also uses

derivatives to facilitate transactions on behalf of its clients. The fair value of derivatives in a gain or loss position

is included in other assets or liabilities, respectively, on the Consolidated Balance Sheets.

BB&T classifies its derivative financial instruments as either (1) a hedge of an exposure to changes in the fair

value of a recorded asset or liability (“fair value hedge”), (2) a hedge of an exposure to changes in the cash flows of

a recognized asset, liability or forecasted transaction (“cash flow hedge”), or (3) derivatives not designated as

hedges. Changes in the fair value of derivatives not designated as hedges are recognized in current period

earnings.

BB&T uses the long-haul method to assess hedge effectiveness. BB&T documents, both at inception and over

the life of the hedge, at least quarterly, its analysis of actual and expected hedge effectiveness. This analysis

includes techniques such as regression analysis and hypothetical derivatives under method 2 of DIG Issue G7 to

demonstrate that the hedge has been, and is expected to be, highly effective in off-setting corresponding changes

in the fair value or cash flows of the hedged item. For cash flow hedges involving interest rate caps and collars,

this analysis also includes consideration of the criteria under the response to question 2 of DIG Issue G20. For a

qualifying fair value hedge, changes in the value of the derivatives that have been highly effective as hedges are

recognized in current period earnings along with the corresponding changes in the fair value of the designated

hedged item attributable to the risk being hedged. For a qualifying cash flow hedge, the portion of changes in the

fair value of the derivatives that have been highly effective are recognized in other comprehensive income until

the related cash flows from the hedged item are recognized in earnings. For qualifying cash flow hedges involving

interest rate caps and collars, the initial fair value of the premium paid is allocated and recognized in the same

future period that the hedged forecasted transaction impacts earnings.

For either fair value hedges or cash flow hedges, ineffectiveness may be recognized in noninterest income to

the extent that changes in the value of the derivative instruments do not perfectly offset changes in the value of

the hedged items. If the hedge ceases to be highly effective, BB&T discontinues hedge accounting and recognizes

the changes in fair value in current period earnings. If a derivative that qualifies as a fair value or cash flow hedge

is terminated or the designation removed, the realized or then unrealized gain or loss is recognized into income

over the original hedge period (fair value hedge) or period in which the hedged item affects earnings (cash flow

hedge). Immediate recognition in earnings is required upon sale or extinguishment of the hedged item (fair value

hedge) or if it is probable that the hedged cash flows will not occur (cash flow hedge).

Derivatives used to manage economic risk not designated as hedges primarily represent economic risk

management instruments of mortgage servicing rights and mortgage banking operations, with gains or losses included

in mortgage banking income. In connection with its mortgage banking activities, BB&T enters into loan commitments

to fund residential mortgage loans at specified rates and for specified periods of time. To the extent that BB&T’s

interest rate lock commitments relate to loans that will be held for sale upon funding, they are also accounted for as

derivatives, with gains or losses included in mortgage banking income. Gains and losses on other derivatives used to

manage economic risk are primarily associated with client derivative activity and included in other income.

Per Share Data

Basic net income per common share is computed by dividing net income applicable to common shares by the

weighted average number of shares of common stock outstanding during the years presented. Diluted net income

per common share is computed by dividing net income by the weighted average number of shares of common

stock, common stock equivalents and other potentially dilutive securities outstanding.

83