BB&T 2007 Annual Report Download - page 124

Download and view the complete annual report

Please find page 124 of the 2007 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

-

136

-

137

|

|

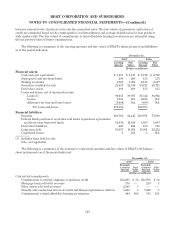

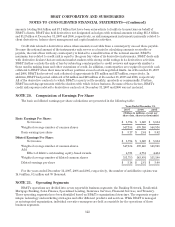

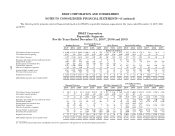

BB&T CORPORATION AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

BB&T utilizes a funds transfer pricing (“FTP”) system to eliminate the effect of interest rate risk from the

segments’ net interest income because such risk is centrally managed within the Treasury segment. The FTP

system credits or charges the segments with the economic value or cost of the funds the segments create or use.

The FTP system provides a funds credit for sources of funds and a funds charge for the use of funds by each

segment. The net FTP credit or charge, which includes intercompany interest income and expense, is reflected as

net funds transfer pricing in the accompanying tables.

Banking Network

BB&T’s Banking Network serves individual and business clients by offering a variety of loan and deposit

products and other financial services. The Banking Network is primarily responsible for serving client

relationships, and, therefore, is credited with revenue from the Residential Mortgage Banking, Financial

Services, Insurance Services, Specialized Lending, Sales Finance and other segments, which is reflected in net

referral fees. Amortization and depreciation expense that has been allocated to the segment totaled $86 million,

$88 million and $83 million for 2007, 2006 and 2005, respectively.

Residential Mortgage Banking

The Residential Mortgage Banking segment retains and services mortgage loans originated by the Banking

Network as well as those purchased from various correspondent originators. Mortgage loan products include

fixed- and adjustable-rate government and conventional loans for the purpose of constructing, purchasing or

refinancing residential properties. Substantially all of the properties are owner occupied. BB&T generally retains

the servicing rights to all loans sold. The Residential Mortgage Banking segment earns interest on loans held in

the warehouse and portfolio, fee income from the origination and servicing of mortgage loans and recognizes gains

or losses from the sale of mortgage loans. The Banking Network receives an intersegment referral fee for the

origination of loans and servicing rights, with a portion of the corresponding charge incurred by the Residential

Mortgage Banking segment and the remaining charge incurred in the corporate office, which is reflected as part

of Parent/Reconciling Items in the accompanying tables. Amortization and depreciation expense that has been

allocated to the segment was not material for any of the years presented.

Sales Finance

BB&T’s Sales Finance segment primarily originates loans to consumers for the purchase of automobiles.

Such loans are originated on an indirect basis through approved franchised and independent automobile dealers

throughout the BB&T market area and, to a lesser extent, states outside of BB&T’s traditional banking footprint.

Sales Finance also originates loans for the purchase of boats and recreational vehicles originated through dealers

in BB&T’s market area. In addition, Sales Finance also provides financing to dealers for their inventories. The

Banking Network receives an intersegment referral fee for servicing the loans originated by the Sales Finance

segment with the corresponding charge remaining in the Sales Finance segment. Amortization and depreciation

expense that has been allocated to the segment was not material for any of the years presented.

Specialized Lending

BB&T’s Specialized Lending segment consists of six wholly owned subsidiaries that provide specialty finance

alternatives to consumers and businesses including: dealer-based financing of equipment for both small

businesses and consumers, equipment leasing, direct consumer finance, insurance premium finance, indirect

sub-prime automobile finance, and full-service commercial mortgage banking. Bank clients as well as nonbank

clients within and outside BB&T’s primary geographic market area are served by these companies. The Banking

Network receives credit for referrals to these companies with the corresponding charge retained in the corporate

office, which is reflected as part of Parent/Reconciling Items in the accompanying tables. Amortization and

depreciation expense that has been allocated to the segment totaled $23 million, $17 million and $14 million for

2007, 2006 and 2005, respectively.

124