BB&T 2007 Annual Report Download - page 13

Download and view the complete annual report

Please find page 13 of the 2007 BB&T annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

|

|

advantageous acquisitions of insurance agencies, specialized lending businesses, and fee income generating

financial services businesses. BB&T’s acquisition strategy is focused on three primary objectives:

Što pursue acquisitions of banks and thrifts with compatible cultures that will enhance BB&T’s banking

network and customer delivery system;

Što acquire companies in niche markets that provide products or services that can be offered through the

existing distribution system to BB&T’s current customer base; and

Što consider strategic nonbank acquisitions in markets that are economically feasible and provide positive

long-term benefits.

BB&T consummated acquisitions of 48 community banks and thrifts, 79 insurance agencies and 31 nonbank

financial services providers over the last fifteen years. In the long-term, BB&T expects to continue to take

advantage of the consolidation in the financial services industry and expand and enhance its franchise through

mergers and acquisitions. The consideration paid for these acquisitions may be in the form of cash, debt or BB&T

common stock. The amount of consideration paid to complete these transactions may be in excess of the book

value of the underlying net assets acquired, which could have a dilutive effect on BB&T’s earnings. In addition,

acquisitions often result in significant front-end charges against earnings; however, cost savings and revenue

enhancements, especially incident to in-market bank and thrift acquisitions, are also typically anticipated.

Lending Activities

The primary goal of the BB&T lending function is to help clients achieve their financial goals by providing quality

loan products that are fair to the client and profitable to the Corporation. Management believes that this purpose can

best be accomplished by building strong, profitable client relationships over time, with BB&T becoming an important

contributor to the prosperity and well-being of its clients. In addition to the importance placed on client knowledge and

continuous involvement with clients, BB&T’s lending process incorporates the standards of a consistent company-wide

credit culture and an in-depth local market knowledge. Furthermore, the Corporation employs strict underwriting

criteria governing the degree of assumed risk and the diversity of the loan portfolio in terms of type, industry and

geographical concentration. In this context, BB&T strives to meet the credit needs of businesses and consumers in its

markets while pursuing a balanced strategy of loan profitability, loan growth and loan quality.

BB&T conducts the majority of its lending activities within the framework of the Corporation’s community

bank operating model, with lending decisions made as close to the client as practicable.

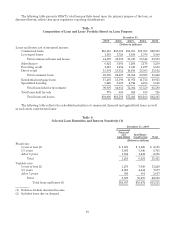

The following table summarizes BB&T’s loan portfolio based on the regulatory classification of the portfolio,

which focuses on the underlying loan collateral, and differs from internal classifications presented herein that

focus on the primary purpose of the loan.

Table 2

Composition of Loan and Lease Portfolio

December 31,

2007 2006 2005 2004 2003

(Dollars in millions)

Commercial, financial and agricultural loans $ 14,037 $ 10,848 $ 9,532 $ 8,824 $ 8,187

Lease receivables 3,899 4,358 4,250 4,170 4,085

Real estate—construction and land development loans 19,474 17,553 11,942 8,601 6,477

Real estate—mortgage loans 44,687 42,219 41,539 39,257 36,251

Consumer loans 11,107 10,389 9,604 9,238 9,208

Total loans and leases held for investment 93,204 85,367 76,867 70,090 64,208

Less: unearned income (2,297) (2,456) (2,473) (2,540) (2,628)

Net loans and leases held for investment 90,907 82,911 74,394 67,550 61,580

Loans held for sale 779 680 629 613 725

Total loans and leases $ 91,686 $ 83,591 $75,023 $68,163 $62,305

BB&T’s loan portfolio is approximately 50% commercial and 50% retail by design, and is divided into four

major categories—commercial, consumer, mortgage and specialized lending. BB&T lends to a diverse customer

13