Humana 2014 Annual Report Download - page 106

Download and view the complete annual report

Please find page 106 of the 2014 Humana annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

|

|

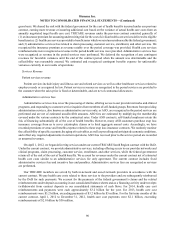

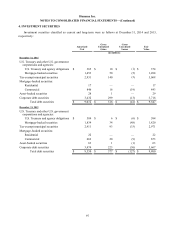

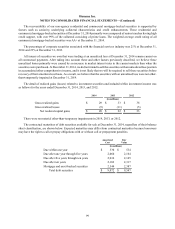

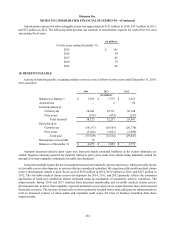

Humana Inc.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—(Continued)

98

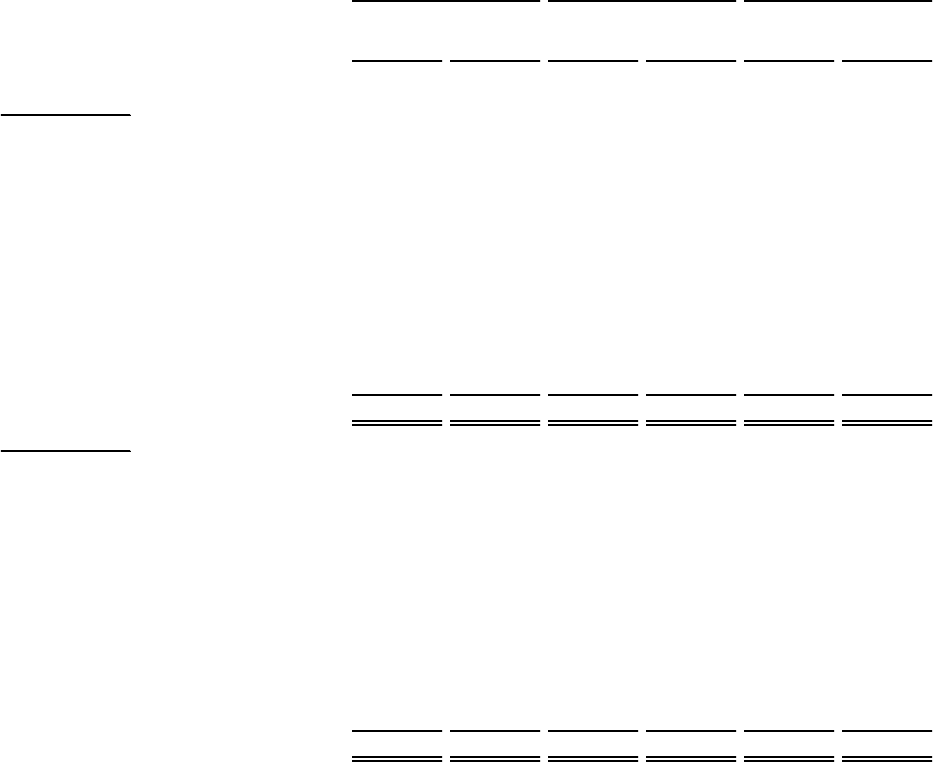

Gross unrealized losses and fair values aggregated by investment category and length of time that individual

securities have been in a continuous unrealized loss position were as follows at December 31, 2014 and 2013,

respectively:

Less than 12 months 12 months or more Total

Fair

Value

Gross

Unrealized

Losses

Fair

Value

Gross

Unrealized

Losses

Fair

Value

Gross

Unrealized

Losses

(in millions)

December 31, 2014

U.S. Treasury and other U.S. government

corporations and agencies:

U.S. Treasury and agency obligations $ 79 $ — $ 80 $ (1) $ 159 $ (1)

Mortgage-backed securities 22 — 320 (5) 342 (5)

Tax-exempt municipal securities 131 (1) 118 (2) 249 (3)

Mortgage-backed securities:

Residential 1 — 4 — 5 —

Commercial 31 (1) 267 (18) 298 (19)

Asset-backed securities 13———13—

Corporate debt securities 219 (6) 128 (7) 347 (13)

Total debt securities $ 496 $ (8) $ 917 $ (33) $ 1,413 $ (41)

December 31, 2013

U.S. Treasury and other U.S. government

corporations and agencies:

U.S. Treasury and agency obligations $ 231 $ (6)$ 5$ —$ 236$ (6)

Mortgage-backed securities 1,076 (47)21 (1) 1,097 (48)

Tax-exempt municipal securities 693 (28)57 (5) 750 (33)

Mortgage-backed securities:

Residential 6 — 1 — 7 —

Commercial 270 (8)40 (1) 310 (9)

Asset-backed securities 35 (1)——35 (1)

Corporate debt securities 594 (28)17 (2) 611 (30)

Total debt securities $ 2,905 $ (118) $ 141 $ (9) $ 3,046 $ (127)

Approximately 96% of our debt securities were investment-grade quality, with a weighted average credit rating

of AA- by S&P at December 31, 2014. Most of the debt securities that were below investment-grade were rated BB,

the higher end of the below investment-grade rating scale. At December 31, 2014, 7% of our tax-exempt municipal

securities were pre-refunded, generally with U.S. government and agency securities. Tax-exempt municipal securities

that were not pre-refunded were diversified among general obligation bonds of U.S. states and local municipalities as

well as special revenue bonds. General obligation bonds, which are backed by the taxing power and full faith of the

issuer, accounted for 36% of the tax-exempt municipals that were not pre-refunded in the portfolio. Special revenue

bonds, issued by a municipality to finance a specific public works project such as utilities, water and sewer,

transportation, or education, and supported by the revenues of that project, accounted for the remaining 64% of these

municipals. Our general obligation bonds are diversified across the United States with no individual state exceeding

11%. In addition, 16% of our tax-exempt securities were insured by bond insurers and had an equivalent weighted

average S&P credit rating of AA exclusive of the bond insurers’ guarantee. Our investment policy limits investments

in a single issuer and requires diversification among various asset types.