Philips 2004 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2004 Philips annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

|

|

Pension costs in respect of defined-benefit pension plans primarily

represent the increase in the actuarial present value of the

obligation for pension benefits based on employee service during

the year and the interest on this obligation in respect of employee

service in previous years, net of the expected return on plan

assets.

In the event that the accumulated benefit obligation, calculated as

the present value of the benefits attributed to employee service

rendered and based on current and past compensation levels,

exceeds the market value of the plan assets and existing accrued

pension liabilities, this difference and the existing prepaid pension

asset are recognized as an additional minimum pension liability.

Obligations for contributions to defined-contribution pension

plans are recognized as an expense in the income statement as

incurred.

In certain countries, the Company also provides postretirement

benefits other than pensions. The cost relating to such plans

consists primarily of the present value of the benefits attributed on

an equal basis to each year of service, interest cost on the

accumulated postretirement benefit obligation, which is a

discounted amount, and amortization of the unrecognized

transition obligation. This transition obligation is being amortized

through charges to earnings over a twenty-year period beginning

in 1993 in the USA and in 1995 for all other plans.

Unrecognized prior service costs related to pension plans and

postretirement benefits other than pensions are being amortized

by assigning a proportional amount to the income statements of a

number of years, reflecting the average remaining service period of

the active employees.

Stock-based compensation

In 2003, the Company adopted the fair value recognition

provisions of SFAS No. 123, ‘Accounting for Stock-Based

Compensation’, as amended by SFAS No. 148, ‘Accounting for

stock-based Compensation – Transition and Disclosure’,

prospectively for all employee awards granted, modified or settled

after January 1, 2003. Under the provisions of SFAS No. 123, the

Company recognizes the estimated fair value of equity instruments

granted to employees as compensation expense over the vesting

period.

For awards granted to employees prior to 2003, the Company

continues to account for stock-based compensation using the

intrinsic value method in accordance with US Accounting

Principles Board (APB) Opinion No. 25, ‘Accounting for Stock

Issued to Employees’.

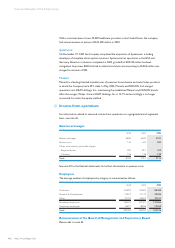

The following table illustrates the effect on net income and

earnings per share as if the Company had applied the fair value

recognition provisions for all outstanding and unvested awards in

each period:

2002 2003 2004

Net income (loss):

As reported (3,206) 695 2,836

Add: Stock-based compensation

expense included in reported net

income, net of related tax (5) 27 52

Deduct: Stock-based

compensation expense

determined using the fair value

method, net of related tax (147) (134) (115)

Pro forma (3,358) 588 2,773

Basic earnings per share:

As reported (2.51) 0.54 2.22

Pro forma (2.63) 0.46 2.17

Diluted earnings per share:

As reported (2.51) 0.54 2.21

Pro forma (2.63) 0.46 2.16

Discontinued operations

The Company has defined its businesses as components of an

entity for the purpose of assessing whether or not operations and

cash flows can be clearly distinguished from the rest of the

Company, in order to qualify as a discontinued operation in the

event of disposal of a business. Any gain or loss from disposal of a

business, together with the results of these operations until the

date of disposal, is reported separately as discontinued operations

in accordance with SFAS No. 144. The financial information of a

discontinued business is excluded from the respective captions in

the consolidated financial statements and related notes.

Cash flow statements

Cash flow statements have been prepared using the indirect

method in accordance with the requirements of SFAS No. 95,

‘Statement of Cash flows’, as amended by SFAS No. 104. Cash

flows in foreign currencies have been translated into euros using

the weighted average rates of exchange for the periods involved.

Cash flows from derivative instruments that are accounted for as

fair value hedges or cash flow hedges are classified in the same

category as the cash flows from the hedged items. Cash flows from

derivative instruments for which hedge accounting has been

discontinued are classified consistent with the nature of the

instrument as from the date of discontinuance.

103Philips Annual Report 2004